Phil Strano, Portfolio Manager of the Yarra Absolute Credit Strategy, details why David Jones’ recent debt deal offers compelling value for credit investors in what remains a weaker bricks-and-mortar retail environment.

It’s been particularly busy in the $A Medium Term Note (AMTN) market in recent months, with several household names taking advantage of conducive market conditions to print large and long tenor deals at very competitive levels. In addition to an inaugural 12-year non-call seven-year Tier 2 issue from NAB ($1.4bn issue), Coles Group (BBB+), Origin Energy (BBB) and Qantas (BBB) all printed 7-10 year deals in October and November ($1.325bn in aggregate) at an average credit margin of ~+160bps.

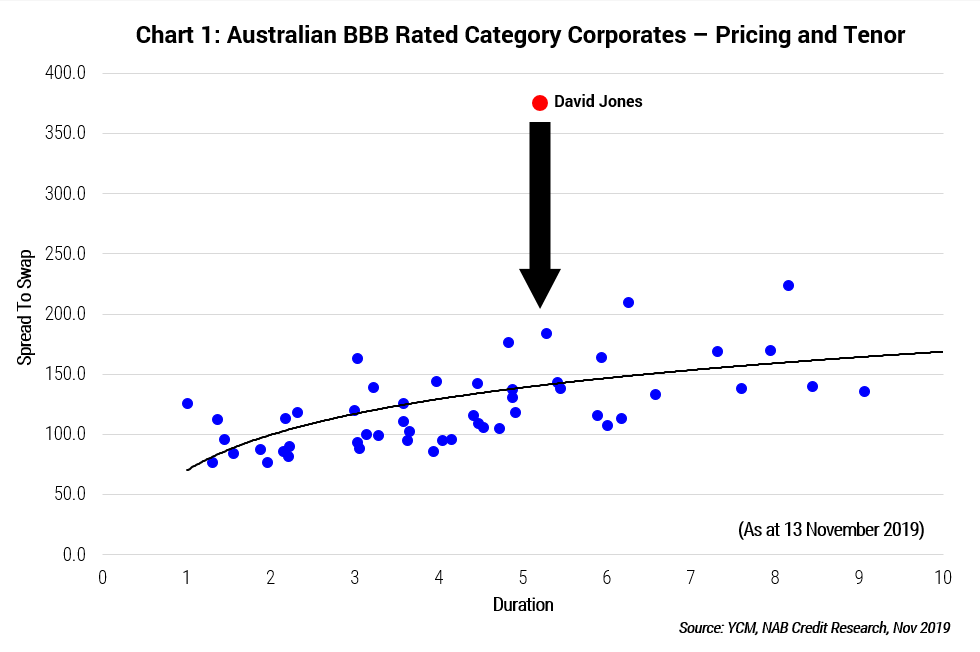

One recent deal which has grabbed our attention came from Australian department store retailer David Jones, wholly owned by Woolworths Holdings Ltd. SA, who this week successfully issued $300mn of 6-year senior secured notes, its first public debt deal for close to 20 years!

Amidst a weaker bricks-and-mortar retail environment, David Jones (DJS) has now restructured its business, reducing its store footprint, renewing its focus on driving online sales (higher margin vs in-store), and opening up new revenue streams (e.g. food/convenience). The retailer is also adding exclusive upmarket brands, including from its wholly-owned Country Road Group (CRG) which owns five well-supported brands in Country Road, Trenery, Witchery, Mimco, and Politix.

Critically, DJS is consolidating each of its freehold Sydney and Melbourne CBD stores and is engaging with its landlords to reduce tenancy costs over the next five years. This comes as no great surprise given the unsustainably high rents in Australian retail, which at 16% of sales are almost a third higher than 15 years ago. Overall, weaker demand for retail space is improving the bargaining power of major retailers who can generate foot traffic, including the broader David Jones Group.

While we remain cautious about the outlook for the Australian retail sector, there is much to like about the structure of the DJS issue with our analysis identifying a large and appealing valuation gap (refer Chart). Yarra’s internal ‘investment grade’ credit rating reflects:

- Our estimate of positive free cash flow from 2020 onwards of ~$50-60mn p.a.;

- First lien mortgage rights over high-quality freehold property;

- Conservative loan to value ratio of less than 50%; and

- Strong covenant protections precluding significant new debt issuance.

In our view, a credit margin of +375bps with a 75 bps BBSW floor for a 6yr note represents compelling value and offers a very significant premium over similar rated Australian investment grade credit.

Our decision to invest in the DJS notes reinforces the benefits of combining a fundamental and independent investment process with a flexible mandate, enabling the targeting of deals offering higher risk-adjusted returns.