As financial markets grind up (or on some exchanges ‘melt up’), it’s worth pausing to dispassionately re-evaluate fundamentals. While the surprise Australian federal election outcome has injected some enthusiasm into the market, the foundations remain fragile. For example:

- Earnings estimates – both locally and globally – have been revised downwards, with Australian (Ex-Resources) earnings revised down 5% over the last 6 months[1].

- Key domestic economic metrics have continued to slip from recent peaks, including GDP (from +3.3% to 2.3% y/y[2]), employment growth (from +3.6% to 2.6% y/y[3]) and various confidence indicators

- Interest rate cuts are now back in play locally (60 bps priced in by Dec 2019) and in the US (30 bps), a response to weakness rather than a bullish signal

- Geopolitical and trade-related issues continue to either fester or escalate, with President Xi now describing the US trade war as “the new Long March” and referencing the need to “win new victories for socialism with Chinese characteristics”

Against this backdrop, valuations continue to stretch and ‘new paradigms’ are being created to value high growth and tech-related businesses. Corporate jargon is often a good indicator: referring to the ‘number of eyeballs’ as a financial metric is out of fashion, while ‘having a large Total Addressable Market’ (“TAM”) is a recent substitute.

The “WAAAX” group – Wisetech Global, Altium, Appen, Afterpay and Xero – is a good case study, rising 77% in the past 12 months, well above the ASX 200’s 13% return. This group of Australia’s tech stocks now trades at an average P/E multiple of 64 times based on two-year forward earnings, a huge premium to US FAANG stocks which trade at a more modest 29 times.

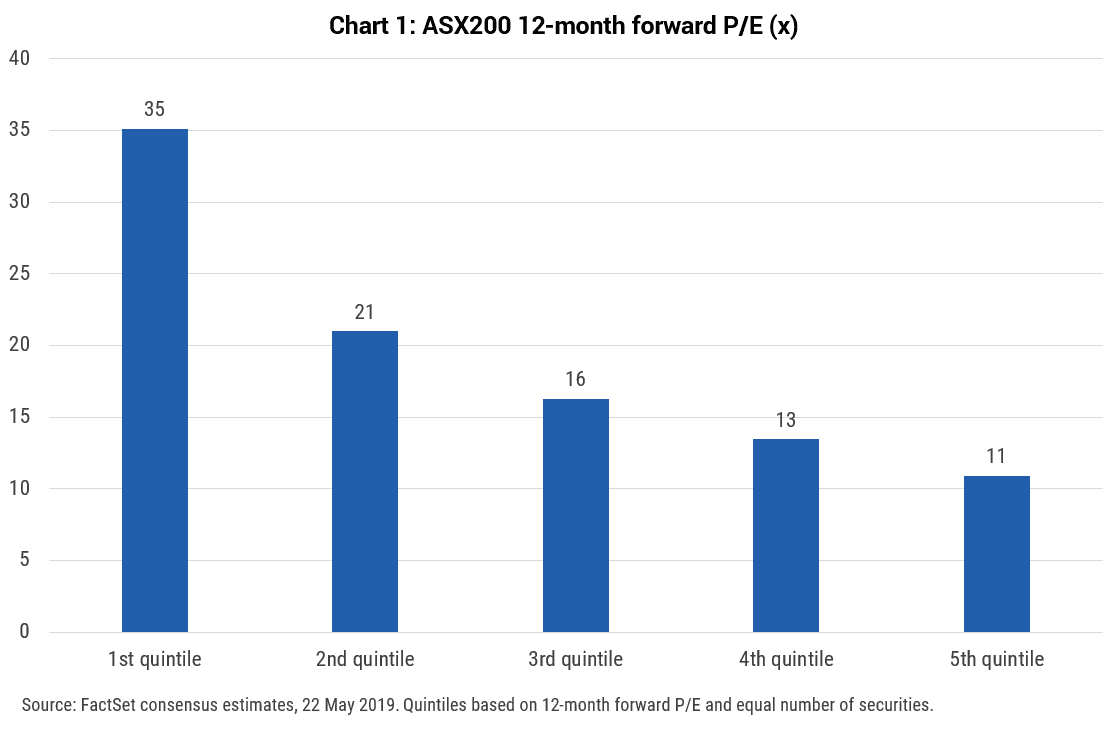

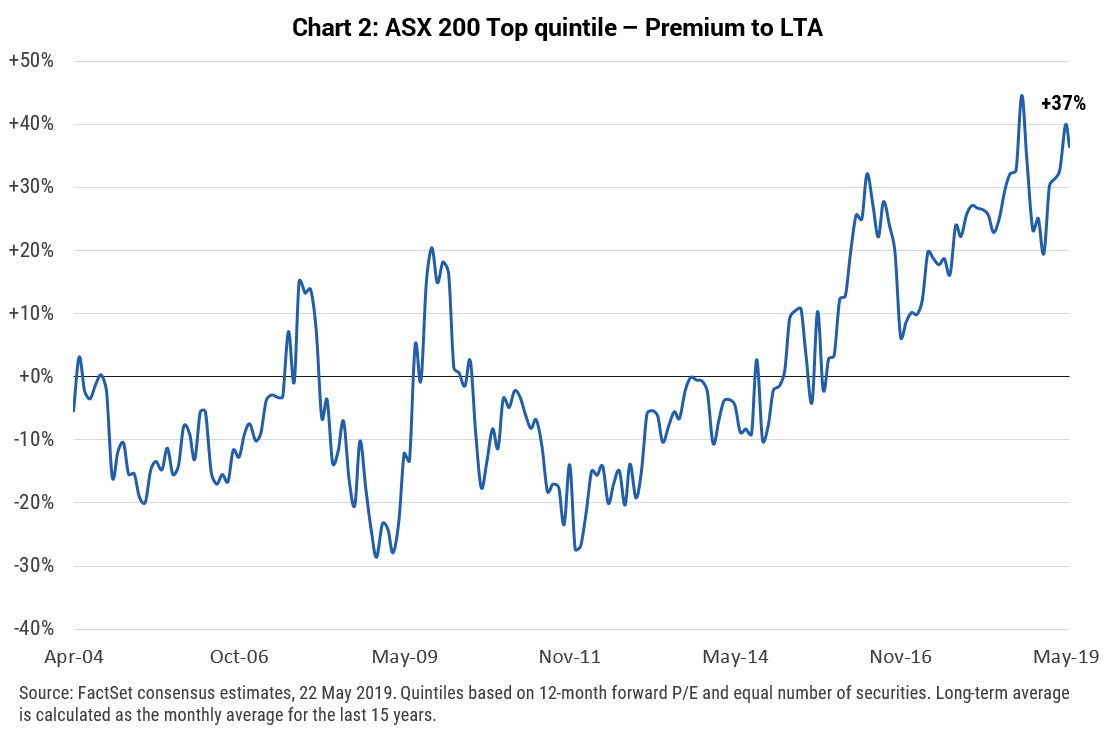

In a market which is probably over-heating, the top quintile of stocks by valuation looks like a furnace. This segment of the market now trades at 35 times forward earnings in Australia – 37% above long-term averages (refer charts). It won’t take much for a large correction to occur.

Despite the post-election rally, we remain conservative against what is a difficult backdrop, relying on ‘old-fashioned’ valuation approaches and using realistic expectations given the outlook.

Great opportunities still exist, but with some qualifications. Patience is required while TPG Telecom (TPM) waits 12 months for the Federal Court to likely overrule the ACCC, and while Origin Energy (ORG) waits for greater regulatory certainty and for its balance sheet to de-lever through strong cash generation. Minor imperfections create opportunities in companies like Incitec Pivot (IPL), which has de-rated over earnings downgrades on seasonal and operational issues that are unlikely to be repeated.

0 Comments