Katie Hudson, Head of Australian Equities Research and Michael Steele, Small Cap Co-Portfolio Manager, take a look at the outlook for Australia’s famed technology sector.

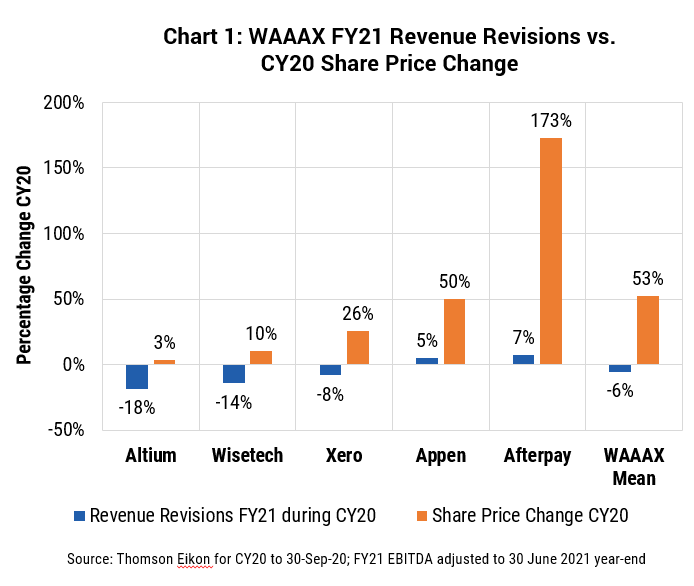

COVID-19 has caused unprecedented and widespread disruption, including to the long perceived safe haven sectors of infrastructure and healthcare. Against this back drop the technology sector has been a significant outperformer with the WAAAX (Wisetech, Altium, Afterpay, Appen, Xero) basket of stocks increasing 53% during CY20, outperforming the ASX 200 by 66%. This outperformance has, at least in part, been driven by a perception they provide defensive growth in this uncertain, low economic growth environment.

However, the resilience of this cohort’s revenue has been sorely tested by the pandemic. In reality many of these companies have cashflows linked to economic activity with exposure to electronic hardware manufacturing (Altium), small and medium size businesses formation (Xero), transport volumes (Wisetech), consumer discretionary spending (Afterpay) and online advertising (Appen). For some, the slowdown has highlighted the revenue was less “recurring” than their high share price multiples implied (Wistech, Altium).

These economic exposures, together with company specific factors, have seen earnings headwinds emerge due to pricing pressure, weaker volumes, slower customer growth and higher cost reinvestment. These factors have resulted in WAAAX consensus FY21 revenue and EBITDA being downgraded by 6% and 19% respectively, which is inconsistent with their perceived safe haven status. Only Appen has been able to maintain consensus revenue and EBITDA expectations during CY20..

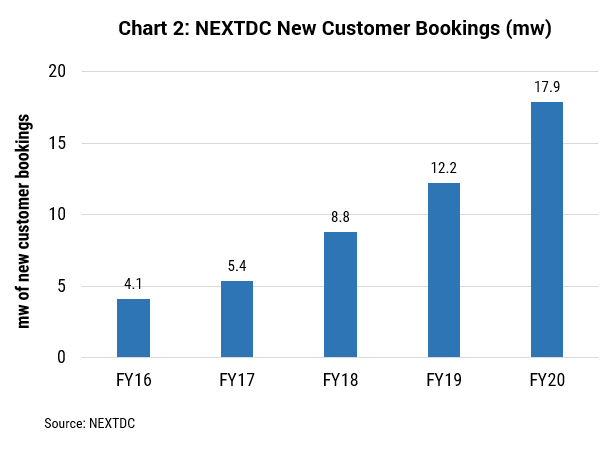

Some tech companies, though, are proving more resilient. The demand for NEXTDC’s product (data centres) has actually accelerated, and unit economics across both price and cost remain unchanged. COVID-19 has driven an accelerated migration to the cloud, in part by the forced shift to WFH across a range of industries. The volume of additional capacity sold during FY20 accelerated materially to more than double the average of the last 3 years. Furthermore, very low churn proved NEXTDC’s revenue to be truly recurring.

We remain underweight the technology sector in our Emerging Leaders portfolio, in particular the WAAAX cohort, but remain invested in a range of technology companies (including NEXTDC) where the growth profile and revenue durability justifies their higher share price multiples.