By Dr Erin Kuo-Sutherland (Chief Sustainability Officer).

The convergence of geopolitical risk, physical climate risk and energy transition is no longer theoretical — and the dominant themes reshaping capital and policy are resilience and security, not substitution. The world must now maintain the fossil fuel system it depends on while building an entirely different energy architecture alongside it.

Energy security and the Energy transition: Two sides of the same coin

For much of the past decade, the energy transition has been framed as a gradual substitution story — fossil fuels declining, renewables rising. That framing no longer holds. Instead, there is a parallel acceleration where the goals of energy security and independence have pointed to a need for diversified energy sources to meet these objectives. Governments are focused on securing fossil fuel supply while simultaneously accelerating domestic energy independence through renewables, storage and, increasingly, nuclear.

These are not contradictory impulses — they are parallel responses to the same underlying problem: that energy security can no longer be taken for granted, and that dependence on any single source or supplier carries risk, including in this current conflict, sovereign risk.

Energy systems built on concentration — whether fossil fuel supply chains or renewable generation profiles — carry equivalent risk. The April 2025 Iberian blackout, caused not by renewables per se but by inadequate grid architecture in a high-solar system, makes this point sharply: resilience requires diversification and system depth regardless of fuel type. The investment case for storage, firming capacity and grid infrastructure follows directly.

Australia’s Energy Paradox: Exporter by Nature, Importer by Design

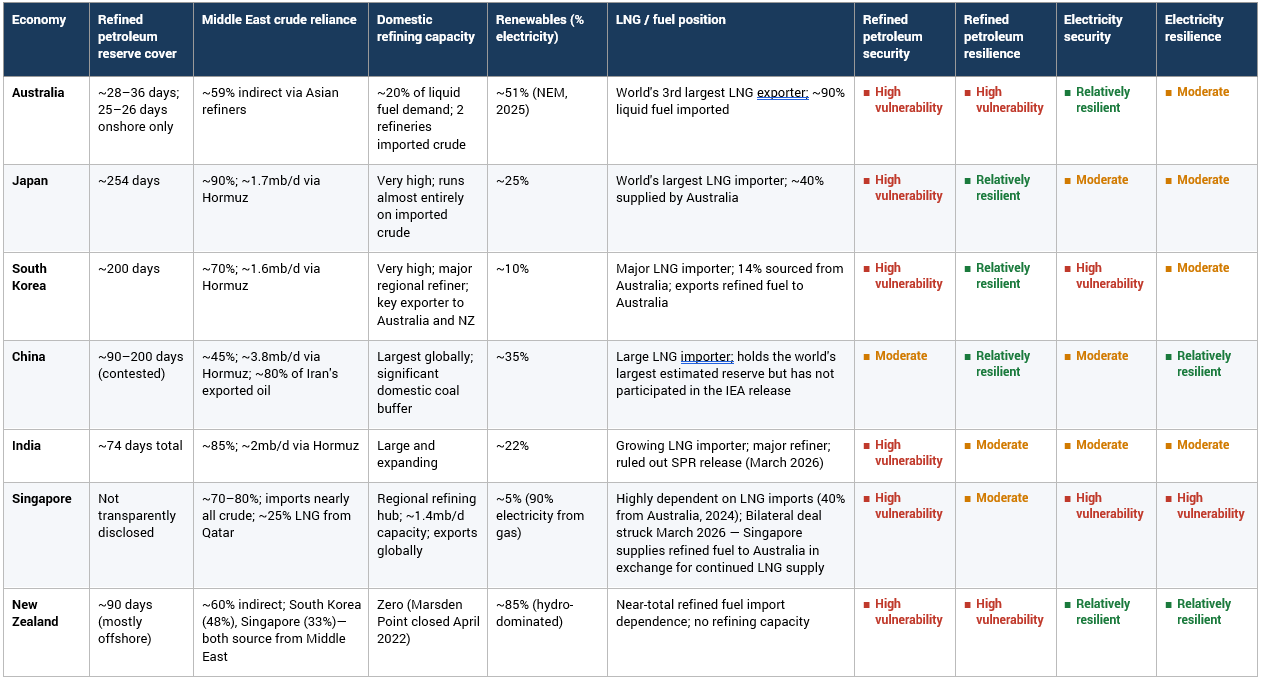

Australia’s energy position is one of the more striking structural paradoxes in the developed world. The country exports approximately 80% of its total energy production[1] — it is the world’s second-largest LNG exporter and a major coal and uranium supplier (Table 1). Yet it imports around 90% of its refined petroleum products and domestically produces just 5.6% of the oil it consumes[2] (a gross figure, representing the share of total liquid fuel consumption met by domestic crude production before accounting for crude exports). It now holds the largest trade deficit in refined petroleum products of any country in the world.[3] While Australia imports negligible crude oil directly from the Middle East, approximately 59% of the crude feedstock used by the Asian refineries it depends on for refined products transits the Strait of Hormuz[4] — meaning, as IEEFA notes, Australia is ‘highly exposed through the Asian refineries we import refined products from[5].

In 2000, Australia was largely self-sufficient in refined petroleum, with eight refineries capable of supplying 98% of domestic fuel needs. Today it operates just two aging refineries — the Viva Energy refinery in Geelong and the Ampol Lytton refinery in Brisbane — with combined capacity covering only around 19% of national demand, and both running on imported crude because Australian domestic output (predominantly ultra-light condensate) is incompatible with their configuration.[6] In 2025 those two refineries covered approximately 19% of national liquid fuel demand — and a small volume of their output, around 4% of production, was exported to Pacific nations without their own refining capacity, making the net domestic contribution marginally lower still. The downstream infrastructure to convert its own resources into domestic fuel simply does not exist at scale. The crisis in 2026 has exposed this double dependency: imported crude for refining and imported finished products, both sourced from the same disrupted region.

The data in Tables A.1 and A.2 (Appendix 1) make clear why the energy security and energy transition arguments have converged. Australia’s domestic energy consumption is 91% fossil fuel dependent. The liquid fuels that account for 41% of domestic energy use are overwhelmingly imported, indirectly exposed to Middle Eastern supply disruption through the Asian refining intermediaries Australia depends on, and held in strategic reserves that are the lowest of any IEA member.

The electricity picture offers a partially more encouraging story. Renewables reached a record 51% of National Electricity Market (NEM) generation in 2025. The 51% renewables milestone in the NEM is genuinely significant — it means that for the first time, more than half of our electricity came from renewables. But electricity is only about a fifth of our total energy use. Fossil fuels still make up over 90% of our total energy consumption, spanning transport, industry, agriculture and gas-fired heat. That’s the gap that makes the transition so much harder than the electricity headline suggests. As we have previously outlined, individual companies are dependent on systemic interventions to decarbonise that reside beyond their direct control — what we have called ‘shared structural dependencies.’[7]

The gap between electricity decarbonisation and whole-of-economy decarbonisation is the most important of those dependencies, and the events of 2026 have made it simultaneously more urgent and more difficult to resolve.

The APAC shock and Australia’s Dual Role

The conflict with Iran has produced what the International Energy Agency (IEA) characterised as the largest oil supply shock in the history of the global oil market.[8] Brent crude peaked near US$120 per barrel in March 2026. In response, the IEA coordinated a release of approximately 400 million barrels from strategic reserves — equivalent to roughly four days of global supply, or around 20 days of disrupted Hormuz volumes — a figure that itself illustrates the scale of the gap.[9] The attack on Qatar’s Ras Laffan facility compounded the impact, reducing approximately 17% of global LNG export capacity with a repair timeline measured in years — and for Australia, a nation that sits uniquely on both sides of the energy ledger, the implications are both immediate and structural.

Australia’s position in this crisis is distinctive within the APAC region. It sits on both sides of the ledger simultaneously — a major energy exporter benefiting from elevated commodity prices, and a domestic economy acutely exposed to those same elevated prices through fuel import dependence. No other regional economy occupies this position in quite the same way, and understanding it matters for how investors interpret the risks and opportunities now emerging.

Table 1 makes Australia’s paradox legible in regional context. Japan and South Korea — the two economies most structurally similar in their import dependence — hold three to five times Australia’s strategic reserve cover and have built deep refining and LNG infrastructure as deliberate sovereign responses to exactly this type of shock. Singapore’s exposure is acute but by design: as the region’s refining hub, price pain is also pricing power. New Zealand sits at the opposite end of the electricity spectrum — 85% renewables — but shares Australia’s vulnerability on liquid fuels: its only refinery closed in 2022, leaving it with zero domestic refining capacity and near-total dependence on imported finished fuel. China’s domestic coal buffer and refining scale provide meaningful insulation that no other regional economy can replicate. The consistent read across the table is that reserve adequacy, refining sovereignty and generation diversity are the three variables that determine shock resilience — and on all three, Australia’s structural position is the weakest of any developed economy in the region.

Table 1. APAC Economy Energy Exposure — 2026 Shock Comparison[10]

Sources: IEA, Nikkei Asia, Black Dot Research, Nation Thailand, Al Jazeera, University of Auckland, MBIE NZ, IEEFA, EIA, Dept of Industry Science and Resources (Aus).

Australia’s trade exposure map (see Table A.4, Appendix 1) reveals a structural irony that the 2026 crisis has made impossible to ignore. Its two most critical fuel import partners — South Korea and Singapore, together supplying the majority of Australia’s petrol, diesel and jet fuel — are themselves deeply exposed to the same Hormuz disruption driving the crisis, sourcing the crude they refine from the Middle East. Malaysia, a third key supplier, has already prioritised domestic fuel needs over export commitments.

On the export side, the LNG Australia ships to Japan, China and South Korea — nearly 90% of its total LNG exports — gives it genuine leverage[11], and the bilateral deal struck with Singapore in March 2026 illustrates the dynamic directly: Australia’s LNG export position is now being used as currency to secure continued refined fuel supply. The arrangement has an additional layer of structural logic: a significant portion of Australia’s crude oil production from Western Australia is exported to Singapore for refining — meaning Australia is in effect buying back its own crude as finished fuel. The March 2026 bilateral deal formalises what is already, in part, an existing supply chain relationship. The two sides of Australia’s energy ledger, long treated as separate, are now explicitly linked — and that linkage is both its greatest vulnerability and its most powerful negotiating tool in the current crisis.

What This Means: Climate Change and the Energy Transition

The transition is not dead — but the conditions under which it was proceeding have fundamentally changed.

The 2026 shock has not killed the energy transition — but it has fractured the political and capital conditions under which it was proceeding. New LNG offtake agreements, fuel storage mandates and refining capacity incentives are all being accelerated by governments responding to supply vulnerability, and each one extends the fossil fuel system’s effective life.

At the global level, the investment picture is more complex than the headlines suggest. Global investment in the electricity sector — generation, grids and storage — is set to reach USD 1.5 trillion in 2025, some 50% higher than total spending on oil, natural gas and coal supply combined, a reversal of the position a decade ago when fossil fuel investment was 30% higher.[12] But that aggregate masks a bifurcation that matters for investors: clean energy investment now accounts for around 67% of total global energy investment, up from 44% in 2015 — yet current levels still fall well short of COP28 targets, with renewable investment needing to double and efficiency and electrification spending needing to nearly triple.[13] The energy security shock has reinforced the investment case for domestic clean energy — not primarily on climate grounds, but on independence grounds — while simultaneously pulling near-term capital toward fossil fuel security.

Three forces are now running in parallel on the transition itself.

First, fossil fuel system maintenance: the world is not abandoning the infrastructure it depends on — it is securing, extending and in some cases expanding it, because the cost of supply failure is now visibly higher than the cost of continued use. China and India approved nearly 115 GW of new coal power in 2024, the highest level since 2015[14] — not a reversal of the transition, but a sovereign risk response by the two economies most exposed to import disruption.

Second, domestic clean energy acceleration: but the primary driver may have moved from managing for climate change to energy independence. Governments that might have moved cautiously on renewables, we are likely to see moving more urgently, because domestic generation is the only form of energy that cannot be disrupted by a strait, a conflict or a refinery fire. In Australia, this was already visible prior to the Iran conflict: battery storage investment reached AU$2bn in 2025, up from AU$90 million in 2017, with 4.9 GWh commissioned in 2025 alone — more than the previous eight years combined[15]. The federal government has since expanded its home battery program from AU$2.3bn to AU$7.2bn over four years, targeting more than 2 million household battery installations by 2030.[16]

Third is grid and system resilience investment. The April 2025 Iberian blackout — triggered by inadequate voltage control and transmission resilience in a high-solar grid — is the clearest signal that the transition’s physical infrastructure is as important as its generation mix. Concentration risk in a renewable system is as real as concentration risk in a fossil fuel system; the mitigant in both cases is diversification, firming capacity and system depth.

More broadly, the crisis is accelerating a repricing of energy infrastructure assets. Wholesale electricity prices across the NEM fell by nearly half to an average of AU$50/MWh in the December 2025 quarter, attributed to record renewable generation and increased battery deployment[17]— a signal that the economics of the transition are working on electricity, even as the liquid fuel crisis deepens. The assets that keep the grid stable and store energy are being recognised for what they always were — essential infrastructure, not optional add-ons. That shift in how they are valued is still in its early stages, leading to opportunities for investors.

Sector Implications

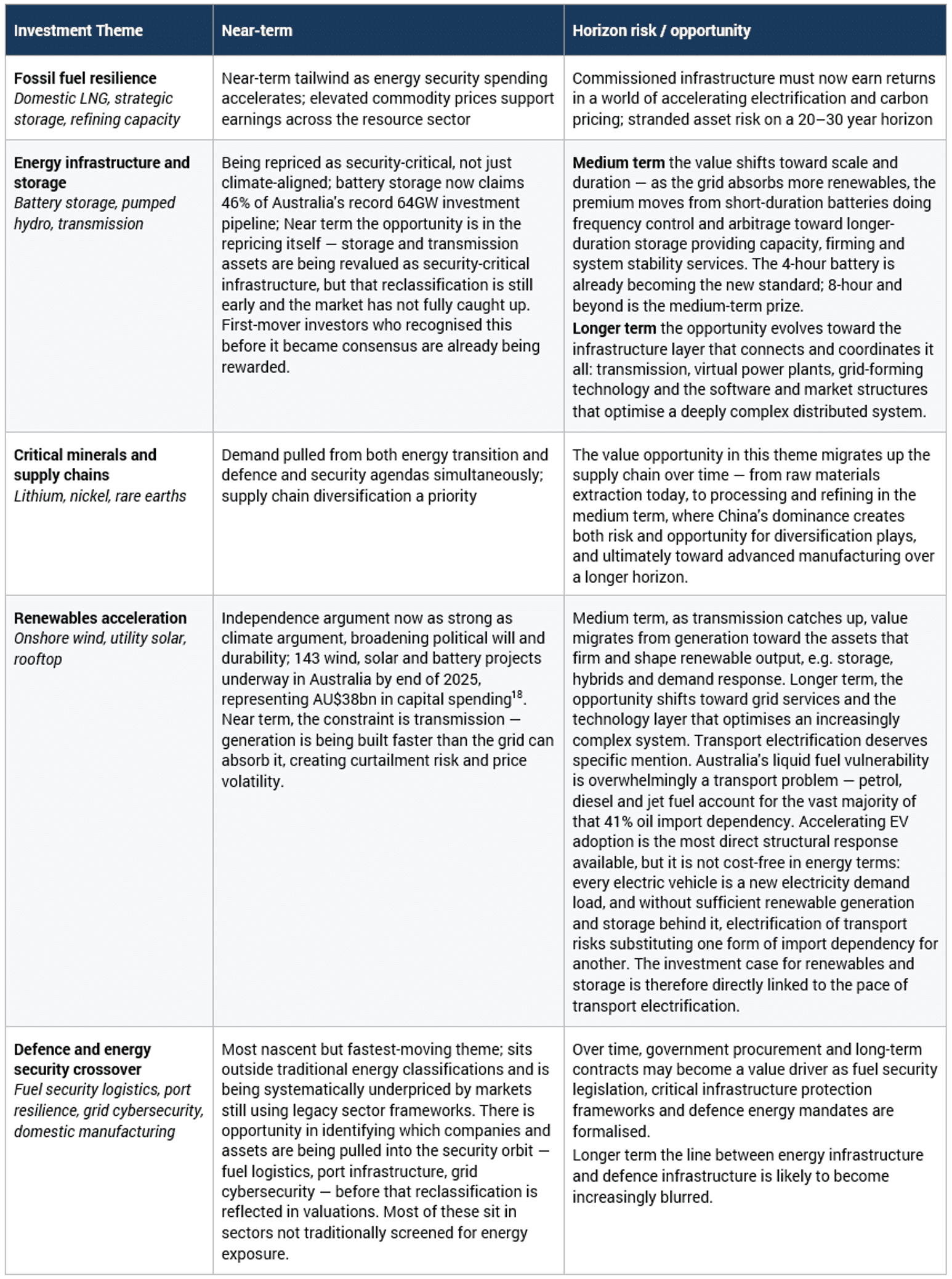

Every major energy shock in the last half century has redirected capital, and 2026 is no different. What distinguishes this one is that the redirection is running in two directions simultaneously: toward fossil fuel security in the near term, and toward domestic clean energy independence over the medium term. The five investment themes below sit at the intersection of both (Table 2).

-

- In fossil fuel resilience, near-term tailwinds for domestic LNG, strategic storage and refining capacity are real, but investors should be clear-eyed about horizon risk — infrastructure commissioned now will need to earn its return in a world of accelerating electrification and carbon pricing.

- Energy infrastructure and storage is a compelling category: battery storage, pumped hydro and transmission assets are being repriced as security-critical, policy support is accelerating, and the investment case no longer depends solely on the climate narrative.

- Critical minerals and supply chains sit at the intersection of the transition and the defence and security agenda. Supply chain diversification away from single-country concentration has become a priority.

- Renewables acceleration is being driven by the independence argument as much as the climate one, which broadens its political durability; the constraint is firming and grid infrastructure, not generation appetite.

- The defence and energy security crossover is the most nascent but a fast-moving theme: fuel security logistics, port resilience, grid cybersecurity and domestic manufacturing capacity are emerging as a distinct and growing investment category that sits outside traditional energy classifications.

Table 2. Five Energy Shock-driven themes and investment horizons

Key Takeaways

1. The organising principles are now resilience, diversification and system depth.

2. Transition assets are evolving: storage, grid infrastructure, firming capacity and some gas assets now qualify under an energy security lens that is politically more durable than a pure climate lens.

3. Stress-test concentration risk at every level — in portfolio construction, in company supply chains, and in geographic exposure; the lesson from both the Iberian grid and the Strait of Hormuz is that concentration without diversification and redundancy is a systemic vulnerability regardless of asset class.

4. Watch Australia’s policy acceleration signals closely: fuel security legislation, critical minerals strategy, domestic storage mandates and grid investment frameworks are all moving faster than the market has priced.

The energy trilemma — security, affordability, sustainability — has reasserted itself with force in 2026, and the comfortable assumption that the transition could be managed as a gradual substitution story has not survived contact with geopolitical reality. The investors best placed to navigate what follows are those who recognise that energy security and the energy transition are not competing objectives — they are, increasingly, the same investment problem.

+++

[1] 19 Interesting Australian Energy Statistics for 2026.

[2] IEEFA, “The Perfect Storm to Boost Australia’s Energy Security,” March 2026.

[3] Ibid.

[4] The refinery problem: A different kind of energy crisis in 2026.

[5] https://ieefa.org/articles/perfect-storm-boost-australias-energy-security.

[6] OilPrice.com, “Australia’s Fuels Dependence Turns Into a Crisis,” March 2026; Riviera Maritime Media, “Australia’s Crude Oil Paradox,” March 2025.

[7] https://www.yarracm.com/australias-climate-transition-where-can-investors-have-impact/.

[8] IEA, Oil Market Report, March 2026.

[9] IEA, Emergency Reserve Release Announcement, March 2026.

[10] Traffic light key: Refined petroleum security = structural import dependency and supplier concentration. Refined petroleum resilience = ability to absorb a supply shock (reserves, substitutability, refining). Electricity security = generation sovereignty and fuel dependency. Electricity resilience = generation diversity, storage and grid robustness.

[11] That leverage carries an emerging domestic policy risk: the debate ahead of the federal budget around taxing gas exports — if legislated — would affect the economics of that negotiating position and represents a sovereign policy risk for LNG sector investors to monitor.

[12] IEA, World Energy Investment 2025, Executive Summary.

[13] Ibid.

[14] Ibid.

[15] Clean Energy Council, Q4 2025 Investment Report; Energy Storage News, Australia commissions 4.9GWh of grid-scale batteries in 2025 (February 2026).

[16] DCCEEW, Cheaper Home Batteries Program (December 2025).

[17] AEMO Energy Storage News, Battery storage claims 46% share of Australia’s record 64GW energy investment pipeline (January 2026).

[18] Clean Energy Council, Q4 2025 Investment Report, as reported in RenewEconomy (February 2026).

0 Comments