How the Australian consumer spends will invariably change as previously closed channels re-open in the post-COVID environment. But for Dion Hershan, Head of Australian Equities, this will not see an implosion in Australian retail.

Out of countless ‘COVID surprises’, the Australian consumer has been the most astounding. Its strength has dragged our economy out of what could have been a prolonged recession (albeit with more than $100bn of federal government support).

A consensus is now forming that the surge in demand was both fortunate and fleeting; a one-time binge as almost 10mn households were locked down and many spending outlets, notably international travel, vanished. The latest forecasts from Deloitte see retail spending slowing to just 0.9% growth in FY22, weighed down by non-food industries such as apparel and household goods retailing. That the consumer may be over-extended – based on higher mortgage debt that is fuelling the housing market – adds to the anxiety.

In contrast, we believe one of the surprises of the second half of this year and 2022 will be ongoing consumer strength. A few simple facts support the case:

- Consumer savings are $223bn higher than they were pre-COVID (in simple terms $23,200 per household);

- The recent drop in the savings rate from 20% in June 2020 to 11% in March 2021 is not the consumer depleting their war chest, but the opposite – they are saving albeit at a lesser rate;

- The wealth effect will be an important psychological driver; average household wealth has expanded by $151k since 1Q2020 (47% of the increase from housing, 30% from Super, 11% from deposits and 8% from direct equity holdings). Typically, for each dollar of wealth, around 4c is spent in subsequent periods;

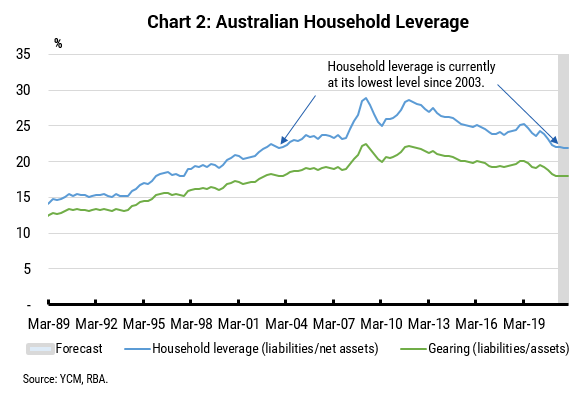

- The consumer has actually deleveraged in the last five years, despite much of the scaremongering you may have read. Asset prices have grown faster than debt and the gearing ratio stands at <20%;

- Low interest (and mortgage rates) seem likely for the foreseeable future (particularly since 44% of new mortgages are fixed) as do tax cuts, and;

- Consumer confidence is always fickle, but at a three-month average of 113 it stands well above the long term average of 100.6.

How the consumer spends will invariably rotate as previously closed channels re-open, but it will not lead to an implosion in retail. We expect the ‘consumer cliff’ to be both distant and also descending from a point much higher than where we are today. We forecast real consumption growth to average 7% in 2021 and 5% in 2022.

We are well positioned in the consumer sector, and actively looking to build our positions if investors become skittish because of like-for-like sales ‘plummeting’ to what we still consider to be strong levels. We are overweight Consumer Services stocks Aristocrat Leisure (ALL) and Star Entertainment (SGR), as well as high-quality retailers including JB Hi-Fi (JBH) and Kathmandu (KMD), the latter of which is highly leveraged to easing international travel restrictions.

0 Comments