Within the fixed income investment landscape, the phrase “there’s no blue sky in credit” is well worn. It reflects a simple economic truth: credit returns are largely fixed at issuance. Coupons and margins are locked in, and unlike equity, debt does not participate in the upside of stronger than expected corporate performance. The quid pro quo is that, when properly structured, credit should also have limited downside if performance disappoints.

Occasionally, however, credit investors are asked to absorb risks that more closely resemble equity. The recent issuance of subordinated notes by data centre owner and developer NextDC (NXT) is a good case in point.

NXT successfully raised $750 million of four-year floating rate subordinated notes at three-month BBSW +350 basis points, equating to a current running yield of approximately 7.85%. After several false starts driven by broader market volatility and concerns around balance sheet stretch, the company was ultimately supported with a substantial $3.2 billion raise in new equity and hybrid capital. That recapitalisation materially improved market sentiment and the deal was comfortably oversubscribed in aggregate.

While we welcome NXT’s return to the Australian credit market, we chose not to participate. In our assessment, the pricing offered insufficient compensation for the underlying risk profile, particularly when set against alternative opportunities across public credit and the syndicated loan market. Past transactions such as Latitude capital notes at BBSW +415bps and the Insignia Term Loan B at BBSW +500bps offered meaningfully superior risk adjusted returns for either comparable or lower levels of credit risk.

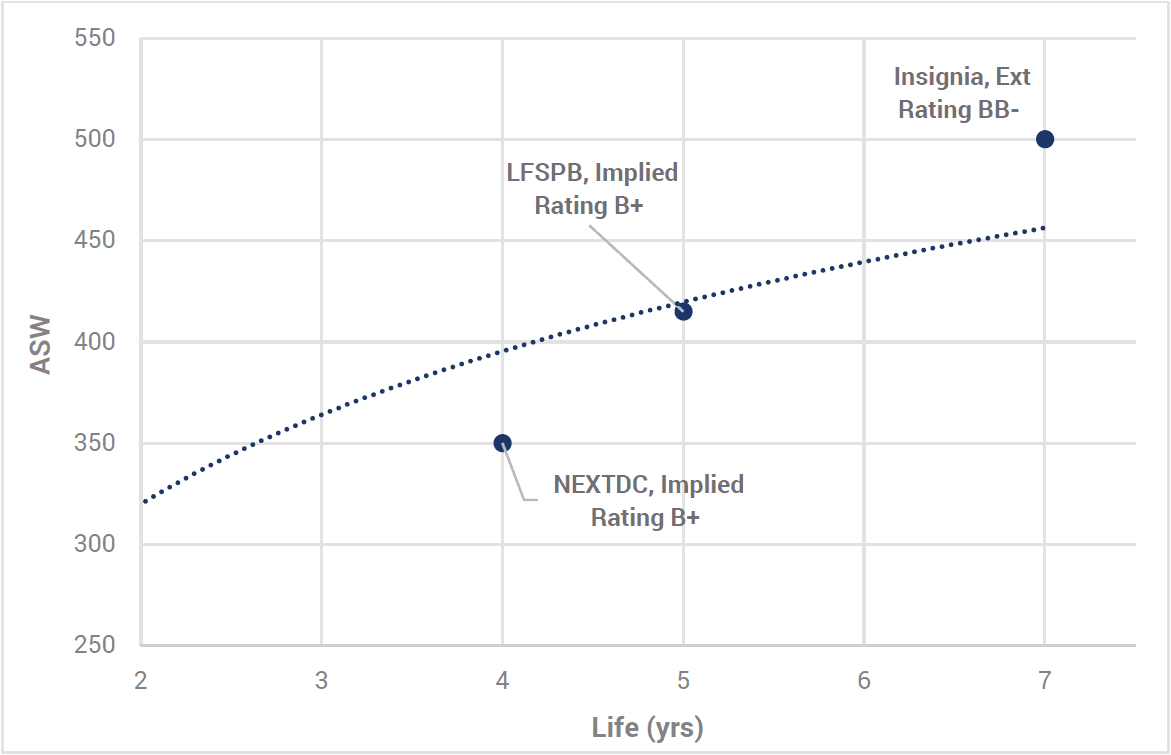

For the NXT subordinated notes, we required an additional 100bps of spread — around BBSW +450bps — to adequately compensate for what we view as a high single B to low double B credit risk profile (refer chart).

Chart 1. NXT vs. recent peer deals

Source: YCM, Bloomberg, Apr 2026.

The core issue lies in the scale and funding structure of NXT’s capital expenditure program. Over the next three years, the company is undertaking one of the largest non-mining capex programs in Australian corporate history, with total balance sheet assets expected to roughly triple by FY28. Management points to a compelling long-term outlook, including projected contracted EBITDA of approximately $1 billion by 2030.

However, the timing mismatch is critical. NXT is building data centre capacity well ahead of revenues, exposing the business to construction delays, cost overruns and execution risk — all in an environment of elevated input costs and uncertain financing conditions. These risks are magnified by management’s decision not to de risk projects through joint ventures prior to construction. Instead, NXT intends to recycle completed assets at a later date, targeting materially higher valuations to maximise shareholder value.

From an equity perspective, this approach may prove highly rewarding. From a credit perspective, however, it introduces a distinctly asymmetric risk profile. Absent further equity issuance or timely asset recycling, leverage is likely to re gear rapidly, with net debt to EBITDA potentially rising well above 10x through FY26–28. Interest cover correspondingly weakens during this period, leaving subordinated noteholders increasingly exposed to adverse outcomes.

In a benign scenario — strong demand, flawless execution and supportive capital markets — asset recycling at premium valuations underpins equity performance. Yet none of that upside accrues to subordinated debt investors. Conversely, in a less favourable scenario involving cost overruns, construction delays, continued high inflation more broadly and/or higher for longer interest rates, both equity valuations and subordinated note values will likely come under pressure.

It is this binary outcome that ultimately shaped our decision. At BBSW +350bps, the risk reward balance appears skewed: investors are being asked to absorb equity-like downside without any participation in equity-like upside. In our view, investors seeking exposure to NXT’s growth thesis may be better compensated owning the shares, while credit investors can find more attractive income opportunities elsewhere.

When appropriately constructing portfolios, the discipline to forgo seemingly attractive transactions can prove the most important aspect of security selection itself. Our decision to not participate in the NXT subordinated issue reflects the rigour underpinning the defensive income generation of our Enhanced Income and Higher Income funds — a discipline that, through the cycle, has contributed to delivering strong risk-adjusted outcomes for investors.

0 Comments