Phil Strano, Portfolio Manager of the Yarra Absolute Credit Strategy, details why he believes the post-pandemic recovery shaping up well for Australian credit investors.

The aftermath of a tumultuous year leaves fixed income investors navigating an environment of very low returns and high uncertainty. Voluminous monetary stimulus around the world has obliterated traditional sources of return and increased underlying risk as interest rate duration lengthens in response to increased government bond issuance.

Talking to investors in recent months, there’s a growing appreciation of floating rate credit and its role in lowering portfolio volatility and growing returns. While allocations to floating rate credit are expected to increase over the coming 12-18 months, the question is which credit markets and sectors offer the best access to higher risk-adjusted returns?

Fortunately, Australian investors needn’t look far, with the post pandemic recovery shaping up well for domestic credit. In fact, paraphrasing Rod Stewart’s anthem ‘Sailing’, there’s compelling value in being ‘home again’. Here’s why:

1. Australian credit is a ~$2 trillion opportunity set – similar in size to the ASX

Australian credit has frequently been viewed as being unsophisticated, with investors often preferencing offshore markets and particularly in higher yielding segments (e.g. US high yield and levered loans). It’s often forgotten is that Australian multi-sector credit (including locally domiciled debt securities issued in foreign currency) is a ~$2 trillion opportunity set, akin in size to the ASX and with countless opportunities to construct multi-billion dollar higher yielding portfolios. Judging from our conversations of late, domestic credit may be losing some of that provincial status.

2. Australia’s superior pandemic performance augurs well for a faster economic recovery

With the pandemic’s second wave now seemingly crushed in Victoria, the Australian economy appears set for a more synchronised recovery. Unfortunately, the same cannot be said for other developed markets. The US, which has just surpassed its daily infection record and is approaching the peak infectious period (i.e. winter), is in a far more precarious position (refer Chart 1). It is a similar story in Europe, with skyrocketing cases driving new lockdown measures across the continent. By virtue of having greater mobility and activity, Australian companies are in a stronger position to service their debt obligations, leaving the domestic credit market well-placed to outperform its offshore peers.

3. Australian credit offers higher risk-adjusted returns in Australian credit than US comparables

Despite its superior pandemic performance, Australian credit on risk-adjusted terms remains more attractively priced than US high yield and levered loans. Our own average investment grade (IG) portfolios have similar credit margins/returns to far riskier US high yield and levered loans. Moreover, despite having a much lower probability of defaulting and higher asset recoveries by virtue of being higher quality, the capital protection (i.e. implied default probability) priced by credit margins is actually higher on our portfolios than US sub-investment grade categories, reinforcing the attractiveness of Australian credit (refer Table 1).

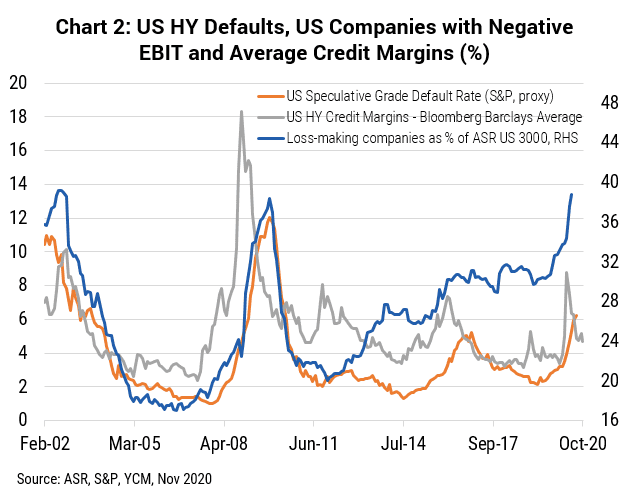

4. US high yield: zombification and lagged default rates

Finally, the so-called zombification of US high yield (i.e. companies accessing debt financing despite in most cases not being creditworthy) and relative tight credit margins (refer Chart 2) are supportive of reallocating into Australian credit. A magnet for global capital due to its reserve currency status and a beneficiary of uber-loose monetary policy, the gap between US companies recording losses and US speculative grade default rates has never been wider. Moreover, both measures are rising rapidly in response to the pandemic, posing a significant risk of much higher US defaults. With fewer excesses, this thematic is not applicable to the Australian market, leaving domestic issuers and our portfolios in a much stronger position to outperform in the years ahead.

The events of 2020 highlight the virtues of Australian multi-sector credit, providing investors opportunities to enhance risk-adjusted returns and generate consistent income of 3.5-4.0% p.a. on highly liquid average investment grade portfolios.

0 Comments