In this note we assess the impact of the 2026-27 Budget, and the risk that in the attempt to engender inter-generational fairness that we create new distortions that ultimately could lead to lower capital investment, lower economic growth. We applaud efforts to remove excessive tax benefits for the wealthy, but if we really want to help younger generations the focus should be on growing the economic pie not disincentivising ‘growth’ capital and distributing the remaining pie into smaller even pieces..

Shifting incentives and unintended consequences

Structural changes to the tax system are not neutral – they materially alter the balance between income and capital, reshape investor behaviour, and ultimately influence both asset allocation and economic outcomes. What looks like a targeted reform to capital gains tax, negative gearing, superannuation, and trusts is, in reality, a broad reallocation of incentives across the entire investment landscape.

Some of this is needed in an effort to address clear distortions. Negative gearing of property and income splitting inside family trusts are clear examples, but when tax policy is used to punish growth capital relative to income strategies, good intentions can lead to poorer economic outcomes

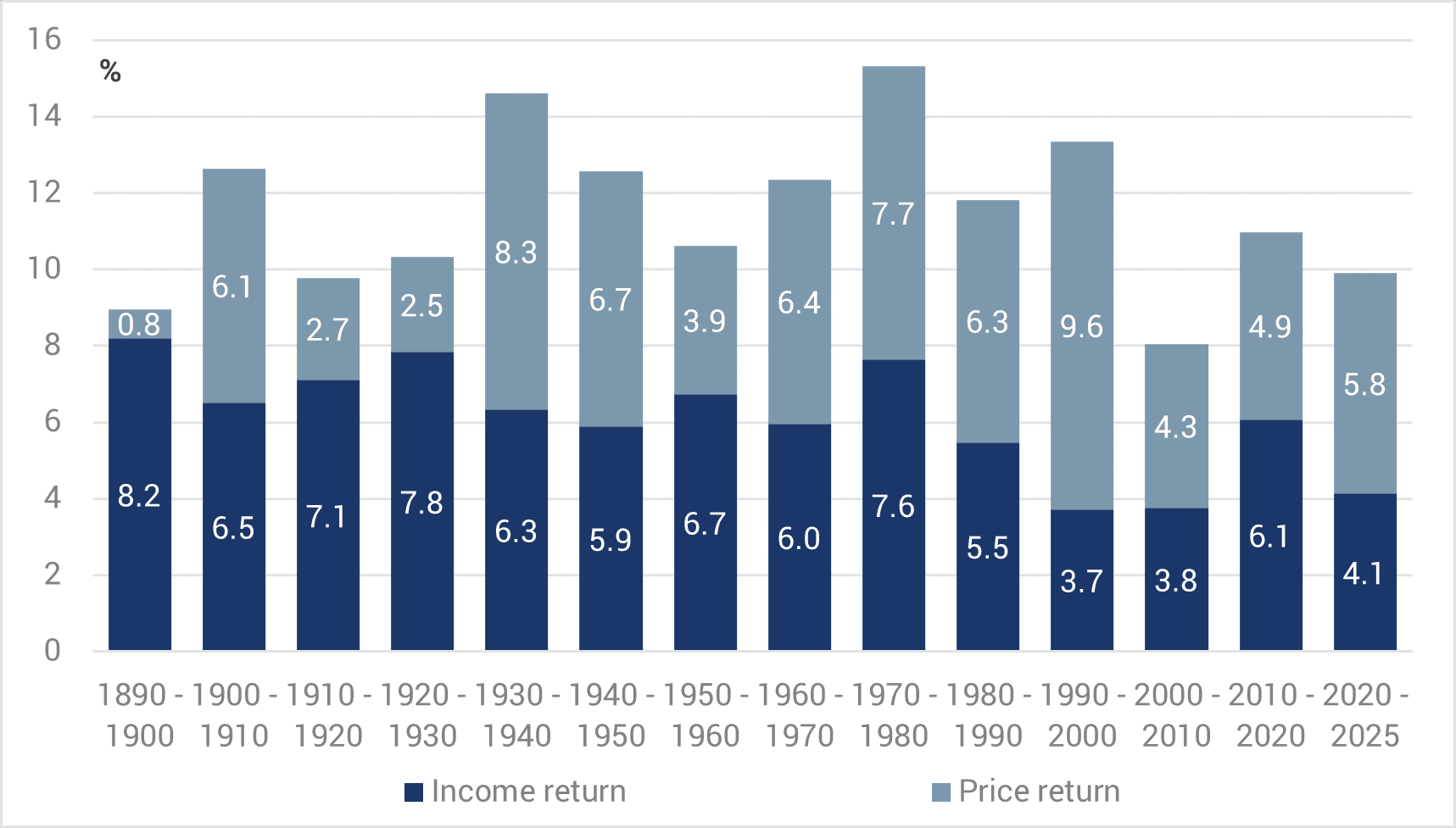

Australian equity returns have historically been a mix of income and capital, but that mix is highly regime-dependent. There have been extended periods where income dominated, periods where income and capital were balanced, and periods – particularly in more recent decades – where capital gains did the heavy lifting thanks to the deregulation, privatisation and trend decline interest rates (refer chart). That distinction matters enormously for tax. If returns skew toward capital and the tax system becomes less concessional on capital gains, effective tax rates rise, even if headline tax rates do not.

Chart 1. ASX200: The Historical Perspective on Income and Price Returns

Source: YCM, May 2026.

Non-indexation of capital losses and the compounding impact over time create major disincentives for ‘growth’ capital

This is the core of the argument around indexation versus the current discount system. Under an indexed system, the tax is applied to real gains, but the absence of indexation for capital losses and the compounding effect of time changes the economics meaningfully. Not indexing losses erodes their real value, increasing tax paid, while longer holding periods expand the effective tax burden. We estimate that if indexation had applied historically, after-tax returns would have been materially lower. For instance, investments in the ASX200 from 1990 would have been ~2 percentage points p.a. lower once non-indexation of tax losses is accounted for. That is quite the change.

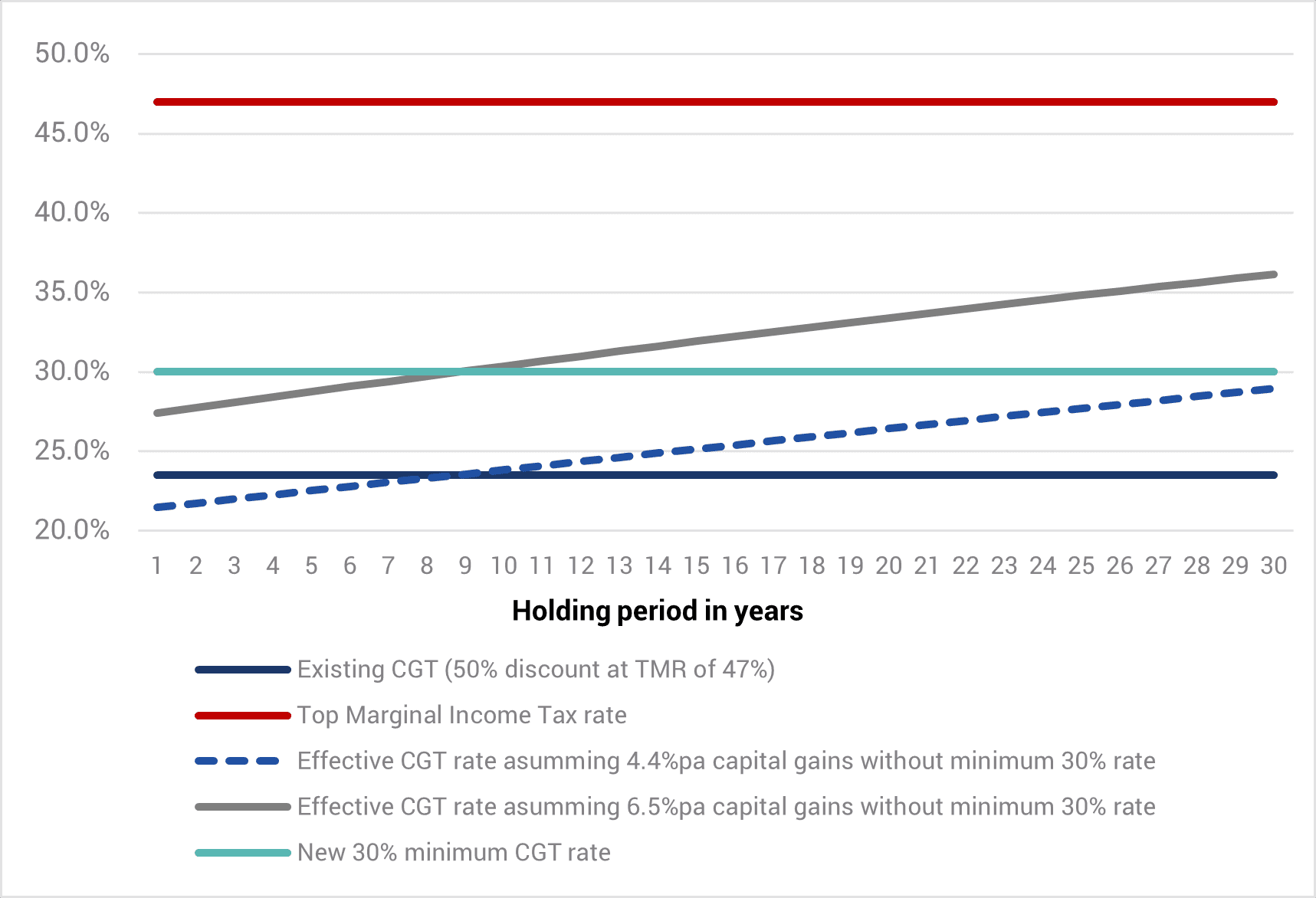

Chart 2. Effective Capital Gains Tax Rates over time for Top Marginal Tax Rate Investors

Source: YCM, May 2026.

Critically, in strong capital growth environments the effective taxation under indexation is much higher. Our modelling suggests that if capital gains average around 4.4% p.a. or more, investors will pay a higher effective tax rate relative to the current regime, assuming an average holding period of 8 years.

This fundamentally alters the risk-return trade-off for growth assets. It obviously penalizes periods of large capital gains but note the investor would have paid less CGT than the existing system if capital gains averaged less than 4.4% p.a. in the absence of the minimum CGT of 30%. However, a 30% minimum CGT means that capital gains would require an average capital gain of a hefty 6.5% p.a. in order to have been indifferent between the two regimes. In other words, even in periods of weak real capital gains growth the ATO slugs the investor regardless of the capital gain at least a 30% rate (and a lot more, relative to the existing CGT discount scheme if the capital gain is >6.5% p.a.).

If you are wondering why such large changes in the CGT regime generate so little forward tax revenue, the reason is that the CGT changes are ‘grandfathered’, new property investors will get to choose between the discount method and the new regime (whichever is more tax effective), and the Treasury coincidently assumes just 4% capital gain p.a. in the forward period. As mentioned above, periods of high capital gains will generate substantial windfall for tax revenue, and in periods of modest capital gains the government still claims its 30% minimum.

In sum, there are three problems with the new proposed regime for CGT compared to the existing system. Under the new regime: (i) the investor pays sharply higher tax in a regime of strong capital gains, (ii) the effective tax burden rises through time when capital gains exceed inflation which penalises holding assets for long periods, and finally (iii) the high 30% minimum CGT is particularly onerous whereby excess tax is paid if asset gains are lower than ~4.4%.

The implication is that an investor in a mature asset owned through the ‘growth’ phase of that asset’s life cycle will be heavily incentivized to sell that asset. An investor’s post tax return on investment diminishes significantly for long-held assets that move into a more moderate growth phase of its life cycle. The new regime penalizes both ‘growth’ capital and long held ‘mature’ capital simultaneously – both of which are essential for stable and growing economy.

Smart political strategy but there are second order impacts worth contemplating

The implications of the Budget changes are quite predictable, and we think significant.

Growth and early-stage investing become structurally disadvantaged relative to income-producing assets. Investors are likely to respond by reallocating: growth assets migrate toward tax-advantaged structures like superannuation, primary homes, and investment bonds, while income assets become more attractive for individuals investing outside of superannuation and those in high-tax brackets.

That is not just a portfolio shift — it is a major change in how capital is allocated within the economy. There may still be some scope for carve-out as the Budget notes it will consult with industry. We might be old-fashioned, but consultation is best done ahead of major policy announcements appear in the Budget Papers. Not afterwards.

There are also second-order effects. Reduced incentives for capital gains could dampen non-superannuation offshore investment outflows and place some upward pressure on the Australian dollar. In a global war for talent, equity-based remuneration compensation structures become less attractive after tax as an Australian taxpayer. And because losses are not indexed, pooled vehicles such as ETFs gain a relative advantage, as they can smooth tax outcomes across investors. Indeed, there is likely an incentive to join newly established pooled investment funds post the changes to avoid the weight of embedded capital gains liabilities.

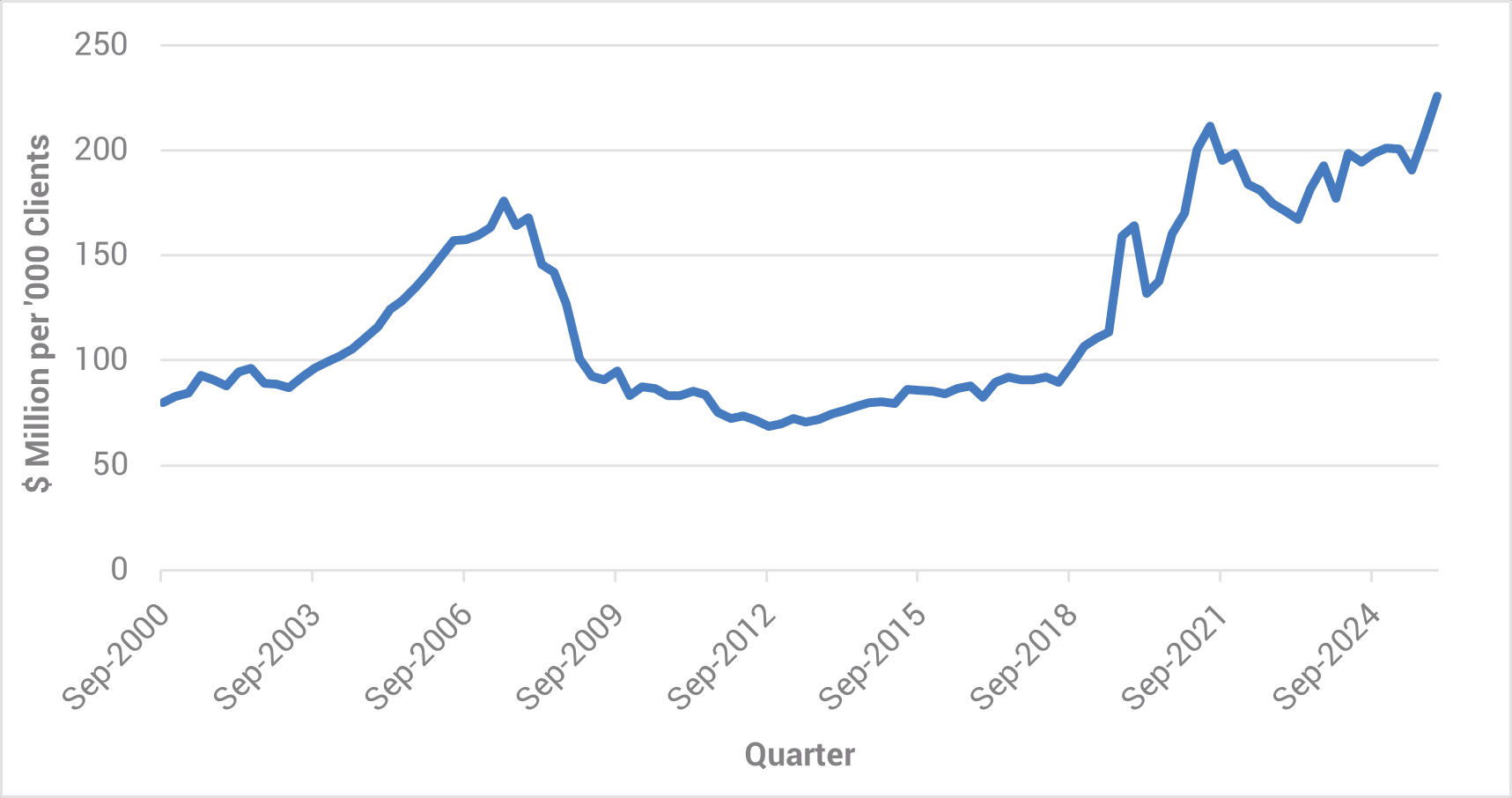

There is also the very real risk that by allowing negative gearing to persist for equity investments, that leveraged tax minimising strategies merely move from a more capital stable asset of housing to a more volatile asset in equities. This could further compress equity risk premia, further increase margin lending accounts and increase the risk profile of household assets.

Chart 3. Average Margin Lending per Client Account Over Time

Source: YCM, RBA, May 2026.

The first order problem is that it reduces the incentive to invest for long periods of time and increases the incentive to consume in the nearer term. Asset rich Baby Boomers, having benefited most from the tax incentives of the past, and are now moving into the retirement phase of tax-free superannuation, tax free family home and grandfathered CGT changes on existing assets and they are now incentivized to load up on franked dividends, sell long held growth assets and lift their consumption. In the generational lottery of life, it seems the Baby Boomers never lose.

Tax changes are not just about fairness. They are about winning votes. The gambit is that with Generation Z and Millennials now a bigger voting block than the Baby Boomers that the path to sustained political power is to appeal to younger voters with some redistributive income policies whilst allowing the Baby Boomers to keep the spoils of their prior wealth generating strategies. Generation X just has to again ‘suck it up’ in the full knowledge they are too small of a voting block to matter. The cleverest thing about the Budget is that to argue against CGT and negative gearing changes has the appearance of arguing against the interests of the young

Changing incentives in Super, Housing and Family Trusts may lead to unintended consequences

The superannuation changes reinforce this theme. Division 296 introduces a step-up in effective taxation for larger balances, taking the rate to 30% for balances between $3 million and $10 million and up to 40% above that threshold. While thresholds are indexed in the newer design, the direction is clear: higher effective taxation of capital within super for larger balances. This tilts incentives, this time within the super system, and again will influence portfolio construction.

For those with superannuation balances under $3 million there is a clear incentive to hold ‘growth’ investments inside of their super fund. For those who exceed $3 million, the incentive skews heavily towards franked income-oriented strategies or tax-exempt investments.

We have no issue with limiting the access to superannuation taxation benefits for high superannuation balances. Indeed, why the Government allows the ATO to cut franked dividend cheques without an upper cut-off limit to the very wealthiest of Australians remains one of life’s great mysteries. The consequence is capital will be on the move for these investors. These investors are likely to be well financially advised and financially nimble in shifting to the next most tax effective structures, including into offshore tax shelters.

Turning to housing, the impact of the tax changes may not be as the Government intends. After the recent run-up in prices the economics of investing in investment property, and using current mortgage rates, outgoings and rental yields, is not cash-flow positive. Aggressive use of depreciation allowances may close the gap somewhat, but on average across Australia it remains negative. In other words, on current inputs the entire investment case for property investors rests on sustained capital gains. Removal of negative gearing incentives obviously makes the equation materially worse. If new policy settings undermine expectations of capital growth, and we think it will, then the asset class becomes significantly less attractive on a standalone basis.

That feeds directly into credit dynamics. Investor loan growth has accounted for roughly 80% of the change in mortgage credit in recent years, meaning the system is highly sensitive to investor sentiment. If expectations of capital appreciation weaken, investor demand could fall sharply. Given the lagged relationship between housing turnover and credit, a slowdown is already likely, but policy-induced changes could amplify the effect. This has clear negative implications for the lending growth of the banks, yet the implications would only be made worse if home prices decline.

Suddenly the conversation becomes more about the prospect of negative equity, delinquencies and provisions. Moreover, the incentive to upgrade the existing rental stock of housing also decreases. If you cannot claim the interest expense, cannot index investment losses and are subject to either lower future house prices or higher capital gains tax relative to the existing system, then why would you renovate? For home building exposed companies, any future benefit from higher new housing investment could be offset by a decline in alterations and additions investment on existing investment.

Importantly, housing investor preferences for established houses verses investment property are not interchangeable, they are more structural in nature. Investors overwhelmingly favour established properties (~85% of property investor capital flows to established homes) for clear reasons: immediate cash flow (avoiding a 12-36 month construction lag), lower execution risk (avoiding developer solvency risk and cost variations), better locations (inner city access to amenities improves capital prospects and lowers vacancy risk), and more reliable financing conditions (banks show a clear bias to lend against an established property with clear peer valuations).

Policies that aim to redirect capital toward new housing must contend with these underlying constraints. While the Government is clearly hoping for the bulk of flow of housing investor capital to merely flow into new housing supply projects, it is more likely that the capital moves to another asset classes that provides better risk, capital growth and tax advantages.

The Budget actually acknowledges that the removal of negative gearing on established property from 2027-28 will lower housing supply by ~30k homes over the next decade. They are merely hoping that prior policies, speeding up approvals and a new $2 billion fund for local government to provide ‘last mile’ infrastructure support will more than compensate. If your council is as efficient as mine, then I wish the Treasury all the best with that assumption. But it is unlikely to materialise.

Indeed, it is worth asking the question, what happens if property investors just keep buying established housing anyway? It is true that they will no longer be able to claim interest expense on established property, however, they may merely opt to run negative income in the early years of the investment and then offset those losses against future income gains.

That is, property investors still get to claim the interest expense as long as they make a positive return in the future. Note that for property investors in established properties, losses are now quarantined against rental income and can no longer be offset against other taxable income. If interest rates remain unchanged, those future income gains can only come via raising rents. In the end it is a similar tax outcome for the Government as the existing system, but it is a worse social outcome for lower income households. Only well-off investors could sustain initial income losses and lower income renters would more likely be the ones facing an escalation in rents. The aspirational middle-class investor would likely not be able to participate at all. Is this fairer?

The discussion of family trusts extends the theme. Taxing distributions at a flat 30% would have wide-ranging implications across those sectors heavily reliant on trust structures – property, construction, professional services, agriculture, and small business. With around 1.1 million discretionary trusts, of which 900,000 are family trusts handling roughly $500 billion in business income annually, the scale is substantial. Changes here are not marginal; they impact the operating model of a large portion of the SME sector. Again, we have no issue with eliminating income splitting techniques used by high income earners, however, some care needs to be taken not to disincentivise the high employing small business sector which suffers from marginal economics at the best of times.

In contrast, the personal income tax changes are trivial in macro terms. A reduction in the marginal rate for lower-income brackets delivers a maximum saving of $268 per year, about $5 per week from 1 July 2026, and a similar amount is scheduled for 1 July 2027. For reference, the cost of large milkshake at McDonald’s is currently over $9. Amanda Vanstone’s infamous criticism of the 2003 tax cut of between $4 to $11 for most taxpayers was that it wouldn’t pay for a “milkshake and sandwich”. This tax cut gets you about half a milkshake in 2026-27 and by 2027-28 the second half of the milkshake will be obtainable. The Government pointed repeatedly to income tax cuts in the Treasurer’s speech, but it is clearly immaterial relative to the broader shifts occurring in capital gains taxation, negative gearing, superannuation and family trusts.

There is a clear Robin Hood undertone to the 2026-27 Budget. The revenue raised by the changes to the way that capital is taxed has largely been redistributed to workers via two new additional sweeteners; the $250 p.a. permanent tax offset for income earned (Working Australians Tax Offset (WATO)) which commences in 2027-28 and a $1,000 instant tax deduction for work-related expenses which commences in 2026-27 worth on average of $205. So, it is clear the Budget is heavy on redistributive policies of taking from the asset rich to give to the working class. But before workers break out in songs of solidarity, we are still talking about just a $17.90 per week post-tax boost after an individual’s tax return is claimed on the 2027-28 year. So perhaps a milkshake and fries. Asset rich households should look at this initiative as the thin edge of a wedge. The Treasurer is referring to the redistribution model from the asset rich to the working poor as the ‘template for the future’. Asset income is essentially being excluded from future income tax cuts under this model.

To be fair, the government has announced a series of measures under its productivity package which includes the re-instatement of two-year loss carry back for all companies with up to $1 billion in turnover, introducing loss refundability (capped at employment-related taxes paid) for small start-ups, making the $20,000 instant asset write-off permanent and expanding tax incentives for venture capital. There is also considerable funding to lower regulation, with construction and environmental regulations receiving particular attention.

At the very small company and start-up phase many of these initiatives are indeed additive, albeit it is difficult to gauge the likely economic success and the payback periods. They also actively encourage a separate tax advantaged investment strategy – early-stage venture capital funds. In other words, wealthy, well-advised investors may have had some doors closed in this Budget, but new tax advantageous doors have also been opened.

Who Wins? Who Loses?

Tax changes can be complicated, but the conclusion for these Budget changes are not particularly complicated.

- Higher effective taxation of capital reduces incentives to invest in ‘growth’ capital, even if some additional new policies help start-up companies at the margin.

- Capital reallocates toward income and tax-advantaged structures. This includes franked dividend streams, primary residence, investment bonds or structures such as tax-exempt early-stage venture capital funds. Bonds may also capture additional flow relative to equities under these changes.

- Housing investment becomes more sensitive to expectations of capital gains. It is feasible that by removing a major marginal buyer in established housing property investors from the market, that established house prices fall, housing turnover falls, and any new housing investment gains are offset by a decline in renovations in the rental stock. This could be problematic for Banks, developers, realtors and even building material companies.

- Mortgage credit growth likely slows materially as investor demand weakens.

- Allowing negative gearing strategies to remain on equities may merely move to equities over property, exacerbating valuation distortions in equities.

- Small business and trust-based structures face higher tax burdens.

The risk is that, taken together, these changes dampen capital formation in a country that has had a multi-decade challenge of boosting capital investment.

Simple economics suggests if you choose policies that penalise investment in ‘growth’ capital, this slows capital formation, slows productivity and lowers future ‘potential’ economic growth.

The best thing policy makers can do for younger cohorts of the population is to ensure there is a tax system that generates strong and sustainable investment, jobs and economic growth. Not reinforce a system that continues to reward franked dividend investing, pouring more capital into the family home and niche investment products. Perhaps changing franking and taxing the family home are not yet on the Government’s menu, but the Greens are certainly salivating for those changes. It will be curious to see what other morsels may be tossed in the Greens direction for this Budget to pass the Senate.

Making a tax system fairer is a desirable aim. But the aim should be to make the economic pie bigger, not to carve the existing pie into even pieces or worse still change the tax recipe so much that it gives growth capital ‘the runs’.

0 Comments