If for some reason you wanted to engineer a hard landing for the Australian economy, what is in the process of being legislated is looking like a very effective playbook.

Although the central bank is of the view the Australian economy has expanded strongly over the past year and is expanding beyond ‘potential’, from our perspective the economy’s momentum peaked in November last year and was demonstrating clear fragility through early 2026 prior to the impact of the oil price shock.

We can debate whether three rate hikes by the RBA were actually required in that environment, since the unemployment rate has now risen a lot more than the RBA thought likely, forward order measures across the economy were in decline and monthly measures of underlying inflation have barely moved despite the biggest oil price shock since the 1970s.

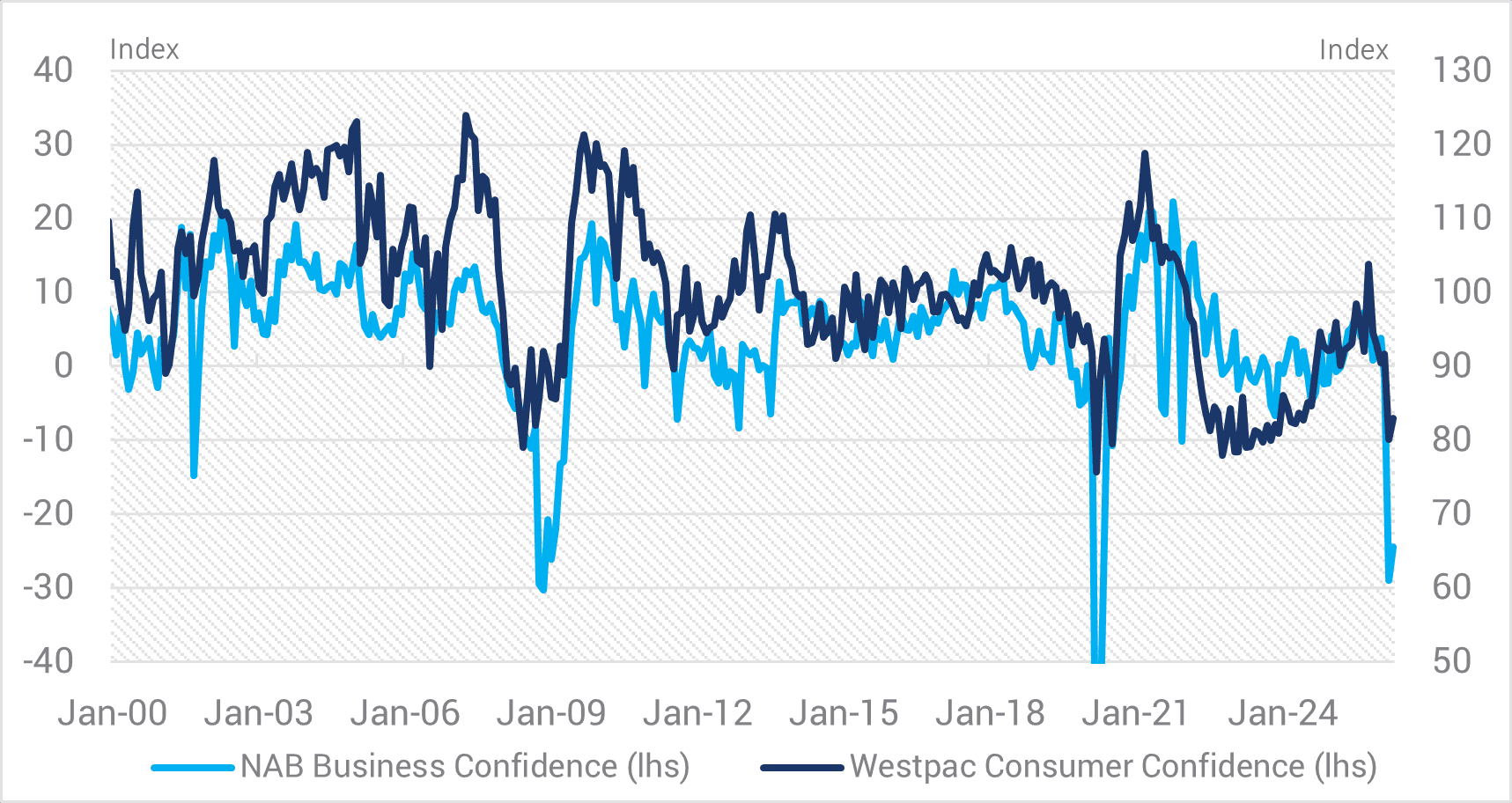

What is clear is that post the oil price shock, business and consumer confidence sits squarely in the toilet (technical phrase, to note they currently are around GFC/Covid crisis levels) (refer chart).

Figure 1. NAB Business Conditions and WBC Consumer Confidence

Source: YarraCM, Westpac, NAB.

Coming into this budget cycle, there was already real fragility in an economy that was on the precipice. Small changes could have tipped the balance; seismic changes are certain to.

The proposed 2026/27 Budget is momentous and has created a consensus in Australia which rarely occurs: one of shock. Irrespective of people’s views on home ownership and the fairness of the existing tax structures, it’s important we don’t introduce a ‘solution that kills the patient’.

The cascading effects of the changes to negative gearing and CGT are profound, complex and there are almost certainly going to be unintended consequences. For the purposes of this discussion, we focus on what we believe they mean for the economy and the ASX:

1. It’s difficult to see a scenario where property prices don’t fall heavily

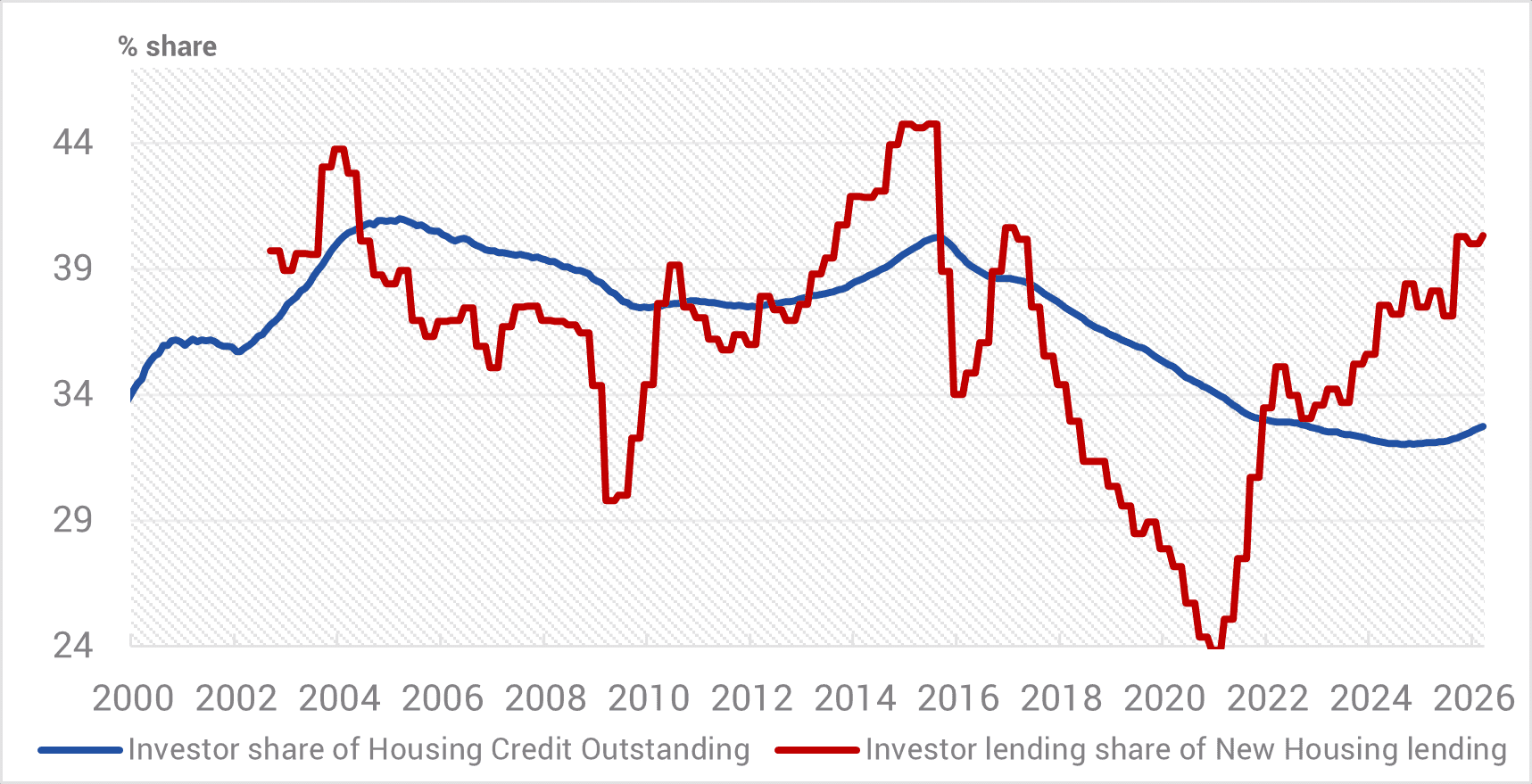

Investors represent approximately 34% of the property market by outstanding credit and by share of the housing stock (refer chart). However, investors currently make up 42% of new housing lending. While investor credit growth had been running at 10% p.a. (vs. system at 7.3%), post the shock of higher interest rates and dramatic tax changes for negative gearing and CGT it is clear that that market has just hit a deep freeze.

Figure 2. Investor Share of House Lending (New & Existing Stock)

Source: ABS, RBA, Yarra Capital Management.

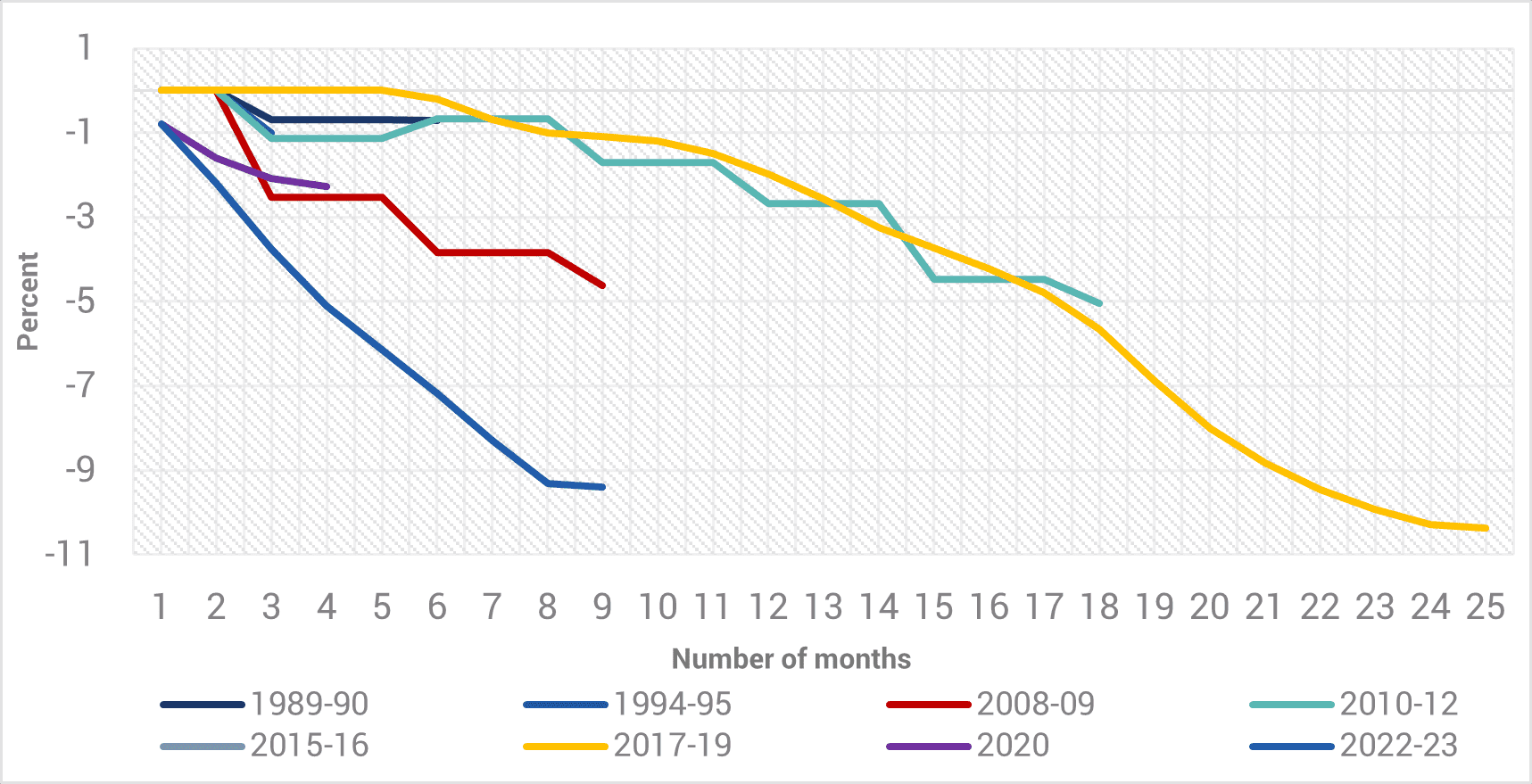

Removing 40% of marginal demand from the buyer pool and creating an expectation of falling prices is likely to cause lenders to recoil and owner occupiers to take a step back (refer chart).

Figure 3. Australian House Price Decline Cycles

Source: Morgan Stanley.

Prior property downturns would suggest anywhere from a 5-15% price drop is plausible, as observed in NZ where investment property changes introduced in 2021, they were the catalyst for a 15%+ correction (those policies were subsequently reversed post a change of Govt. in 2025). With inflation well above target, the RBA cutting rates and bailing out property (as has happened in the past) seems very unlikely short to medium term.

2. Falling property prices will further damage consumer confidence

It’s pretty simple maths: with about 60% of consumer net worth tied to residential property (ABS), falling prices have an adverse wealth effect and are extremely likely to hit consumption and drive a lift in the savings rate.

3. Housing starts & rents are likely to move in the wrong direction

Irrespective of the budget’s objectives, hidden in plain sight is a view that housing starts are likely to be 35,000 lower over the next decade and rents are likely to grow by 4% p.a. in the near term. For investment property to generate equivalent cash returns post the tax changes, rent increases above 30% would be required. Both of these moves will have an adverse economic impact.

4. CGT changes will dramatically re-shape investor preferences

Anyone in markets will tell you that capital flows to where it can achieve the highest risk-adjusted, after-tax returns. By effectively doubling the capital gains tax rate on high-risk investments (e.g. venture capital, early-stage mining, biotech etc.) you will crowd out investment – it’s not merely an opinion, its math.

Investments will now likely flow into lower risk term deposits, fixed income, and the franked dividend streams of blue-chip large cap equities etc. At the risk of stating the obvious, putting money in a term deposit, an ANZ hybrid or Westpac shares simply doesn’t create jobs or add to GDP. Backing start-ups or junior mining companies to develop mines, however, creates jobs and GDP and is a large economic multiplier.

Listed companies could also become even more risk averse and favour higher dividend payout ratios rather capex, M&A or share-buy backs that are more likely to be subject to CGT.

5. The Sacred Cows (for now) are also likely to attract more capital

The Budget left the tax status on your primary place of residence (CGT exempt) and super (sub-$3m) unchanged. It stands to reason that they will take a larger share of future savings, but again we make the point they are not large economic force multipliers that create jobs and GDP growth.

6. The changes could well ‘dumb down’ the ASX even further

As we have consistently maintained, the ASX 200 already has an unhealthy level of concentration (top 10 stocks are ~50% of the market).

The proposed tax changes will push more money into blue-chips and more money into index linked funds (away from direct stock ownership, in particular higher risk stocks). Worse still, the changes will only reinforce the large unintended consequences associated with the implementation of the Your Future Your Super reforms that have made industry funds far more benchmark aware and large cap stocks more overvalued. Creating greater herding around large cap ASX stocks and reducing diversification is unlikely to be in investor best interests.

7. The unintended downstream implications could prove significant

By way of example, with the residential property market likely to go into a deep freeze as investors withdraw from buying and prices fall, the impacts are likely to be compounded further as investors hoard the negatively geared properties they already own (as they won’t be able to negatively gear existing properties again).

Accordingly, it’s likely that housing turnover will drop 20-30% in the medium-term. In Victoria (and likely similar in other states), stamp duty represents around 20-25% of tax revenue and is likely to come under intense pressure as housing turnover steps down. If payroll tax and land tax are used to compensate it could further damage a fragile state economy (which is 25% of national GDP).

Although these themes might appear alarmist and pointing to a hard landing seems emotive, it has to be actively discussed. It’s worth reflecting on that the fact the investment property ownership changes in NZ in 2021 (which were more similar than different to what is proposed) were a major contributing factor to the economic contraction that followed and subsequent economic malaise.

These profound proposed negative gearing and CGT changes are projected to create <$3bn p.a. of tax revenue by 2030 (by way of comparison, tobacco excise taxes have dropped by $12bn p.a. since 2019). This is a mere 40 bps of total tax revenue and makes hardly any space to fund meaningful tax cuts which will almost certainly be needed to stimulate what is likely to be a distressed consumer.

0 Comments