By Dr Erin Kuo-Sutherland (Chief Sustainability Officer).

The climate transition introduced investors to the concept of the ‘just’ transition: the recognition that decarbonisation carries social costs, particularly for workers and communities dependent on fossil fuel industries. Labour displacement became a central political and investment constraint, and in some cases concerns about job losses have been used to slow or reshape the shift away from fossil fuels. Importantly, in the climate transition, governments have largely set the pace and rules of change — through policy, regulation and market design.

Artificial Intelligence (AI) reframes that debate. Unlike the climate transition, where governments have largely set the pace and rules of change, the AI transition is being led primarily by the private sector, with less coordination and policy visibility. This is creating a more decentralised and potentially more complex transition dynamic.

The AI Transition is Creating New ESG Trade-Offs

Unlike the climate transition — where environmental goals have often collided with employment concerns — the AI transition is largely driven by productivity and efficiency gains. Yet those gains come with their own externalities: rising energy and water demand, large-scale labour displacement in certain sectors, and new governance risks tied to algorithmic decision-making and technology concentration.

For investors, this creates a new form of ‘just’ transition challenge. The trade-off is no longer between environmental progress and jobs, but between productivity gains and the environmental and social costs embedded in AI adoption.

AI Infrastructure is Driving New Energy and Water Constraints

AI’s environmental footprint is becoming increasingly visible in electricity markets. Recent estimates suggest a generative AI query can use between 5–10 times the electricity of a standard internet search, depending on model complexity and usage[1]. In Australia, there are already more than 250 data centres nationally, with capacity expected to grow at least fourfold by 2035[2]. Oxford Economics estimates that data centres in Australia currently consume ~2% of grid electricity but that share could triple within five years[3].

This demand arrives at a time when the National Electricity Market is already undergoing a complex structural transition, retiring coal generation while integrating large volumes of intermittent renewable supply. AI-driven demand is emerging as a meaningful new load source — with hyperscale data centres potentially requiring up to 1GW each, equivalent to the electricity demands of a small city[4]. The result is a new layer of demand pressure on an electricity system still building the firming capacity required to support renewable generation. This creates a tension with climate objectives: AI-driven demand may extend the life of fossil generation or increase reliance on gas peaking capacity if renewable firming lags demand growth.

For investors, the implications vary across sectors. Electricity generators and network infrastructure providers may benefit from a structural demand tailwind. Utilities including AGL and Origin Energy could see improved demand visibility, while transmission and pipeline owners may benefit from requirements to expand grid infrastructure.

Data centre operators sit at the centre of this transition. Companies such as NextDC are direct beneficiaries of AI infrastructure demand, but their investment case is increasingly linked to energy procurement strategy. Long-term renewable power purchase agreements, grid access and electricity price volatility are becoming critical operating variables.

Water adds another, less visible constraint— but one increasingly shaping social licence dynamics. Hyperscale data centres relying on evaporative cooling can consume well over one million litres of water per day[5]. In some Australian cases, proposed facilities have requested up to 40 million litres per day, placing direct pressure on municipal systems[6]. However, this varies significantly by design, with many newer facilities increasingly using recycled water, air cooling or closed-loop systems to reduce potable water intensity[7].

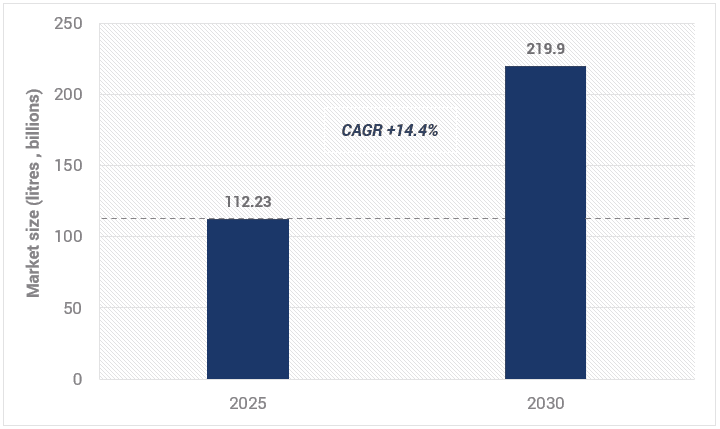

Current water usage remains relatively modest but is rising rapidly, with ~3.5 billion litres per year already used by data centres in Sydney (<1% of supply)[8] but projected to rise to ~25% of Sydney’s water supply by 2035 under some scenarios[9]. At a national level, data centre water consumption is currently estimated to be ~112 billion litres in 2025, projected to rise to ~220 billion litres by 2030[10] (refer Figure 1).

Figure 1. Australian Data Centre Water Consumption Projections

Source: Mordor Intelligence.

This is becoming a clear social licence issue since:

- Data centres often rely on potable (drinking) water in water-stressed regions;

- Demand is concentrated in urban growth corridors already facing climate variability and population pressure; and

- Policy frameworks for water allocation have not kept pace with AI-driven demand growth.

This has already triggered regulatory attention, with water authorities calling for national standards and greater transparency on data centre water use.

AI Productivity Gains Come with Workforce Transition Risk

There is a wide degree of uncertainty over job displacement from AI, with some estimating ~50% of tasks across developed economies could be automated or augmented by AI over the next decade[11]. Research from the CSIRO and the Reserve Bank of Australia suggests a significant share of the Australian workforce is concentrated in occupations exposed to automation[12]. Financial services, insurance, professional services and public administration — sectors representing a large share of ASX market capitalisation outside resources — contain many roles susceptible to AI-driven task automation.

AI offers a powerful productivity lever. Labour costs represent a significant share of operating expenses in service sectors — exceeding 50% in labour-intensive industries such as financial and professional services firms, where automation has the potential to improve margins over time.

On the other hand, workforce transitions are rarely frictionless. Redundancy payments, retraining programs and corporate restructuring costs may emerge before productivity gains are realised, creating transition costs not yet fully reflected in valuation models or earnings forecasts.

The social licence dimension may prove equally important. Some large employers maintain back-office operations in regional centres where alternative employment opportunities are limited. Rapid workforce reductions in those communities could trigger reputational and regulatory responses more quickly than financial models assume — with parallels to past governance failures where automated decision-making led to adverse social outcomes (e.g. the Robodebt Royal Commission[13]). Regulatory scrutiny is also increasing as policymakers examine how automated decision-making intersects with employment law and worker rights.

AI is Creating a New Technology Concentration Risk

Governance remains the least visible dimension of the AI transition, yet it may ultimately prove the most material financially.

Many Australian companies deploying AI are becoming operationally dependent on a small number of global technology providers. This creates a new form of supply chain concentration risk.

At the same time, regulatory expectations around AI governance are evolving. Technology risks, including data breaches and algorithmic bias, are increasingly understood as falling within directors’ duty of care. Importantly, biases embedded in AI systems can influence outcomes at scale — creating legal, reputational and regulatory risks that may not be fully captured in current governance frameworks. Privacy law reforms and growing scrutiny around automated decision-making may further expand corporate liability exposure.

Despite these developments, AI governance risks, like many ESG risks, are difficult to predict and price. This may leave investors carrying unrecognised risk.

AI Transition Framework

Governance remains the least visible dimension of the AI transition, yet it may ultimately prove the most material financially.

Viewed through an ESG lens, the AI transition can be understood through three interacting variables:

- Productivity opportunity — efficiency gains and margin improvement from automation;

- Labour transition risk — social licence, regulatory and restructuring costs; and

- Resource intensity — energy and water demand.

Overlaying these variables is a governance dimension, including technology concentration risk, board oversight of AI deployment and evolving regulatory expectations around automated decision-making.

Table 1. AI Transition Framework

Investment Implications

Few sectors sit cleanly along one dimension. Major banks, for example, combine significant productivity opportunities with high labour displacement exposure. Utilities may benefit from rising electricity demand but face decarbonisation pressures as data centre loads increase.

The near-term opportunity lies in identifying companies able to capture AI productivity gains while managing resource intensity and workforce transitions. Firms that treat workforce transition planning, energy procurement and resource management as strategic issues rather than afterthoughts are best placed to ultimately generate more durable value.

Investors should pay close attention to labour-intensive companies adopting AI rapidly without a workforce transition strategy. Large workforce restructurings may introduce transition costs and operational uncertainty that could impact stability and investor confidence. AI should not simply be treated as another ESG risk factor. It represents a structural transition that reshapes how environmental resource use, labour markets and governance risk interact across the economy.

For responsible investors, the just transition debate is no longer confined to coal communities and energy markets. It is now unfolding across the digital economy —particularly in major cities where AI infrastructure, labour markets and resource constraints intersect most directly. Those that recognise this shift early — and integrate it into investment analysis — may find both risks and opportunities emerging well before markets fully price the transition.

0 Comments