Phil Strano, Portfolio Manager of the Yarra Higher Income Fund, details why investment grade credit appears well placed to outperform the high-yield and private debt segments.

Increased volatility is seemingly the dominant theme for 2022, with higher inflation, sharply escalating interest rates –incl. domestically with the RBA’s 50bp rise last week – and prolonged supply chain disruptions from COVID and the Ukraine/Russia conflict all contributing factors.

Through the back half of 2020 and into the first half of 2021 we have been wary of the re-emergence of higher rates and vulnerability of longer interest rate duration assets (e.g. traditional fixed income). While not surprised by the duration sell-off, its magnitude has surprised, with the Bloomberg Composite Index down ~8% year-on-year. By contrast, the total return from the Bloomberg Credit FRN Index – which is of inferior credit quality but has much shorter interest rate duration – is down just 0.16% over the same time frame (refer Chart 1).

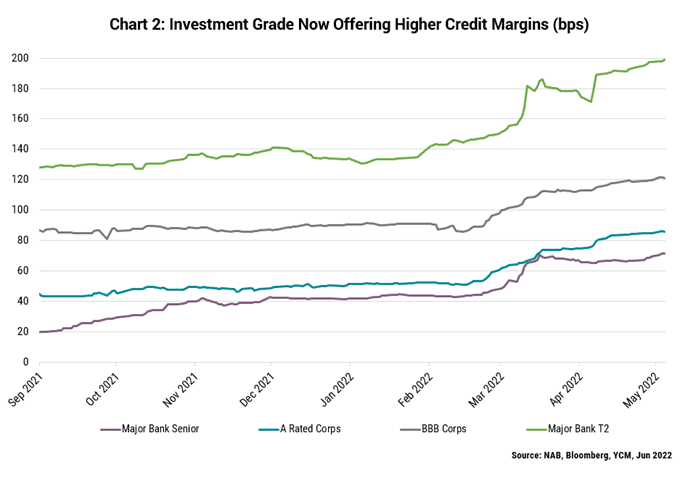

For credit, the movement higher in yields has not been confined purely to risk-free rates. Investment grade (IG) credit margins in public markets across high quality financials and corporates have also widened by an average ~50bps from their late 2021 lows (refer Chart 2).

Certainly, in our view, the movement wider in credit margins has restored value to high-quality credit, with recent issuance providing tangible examples of the attractive returns currently on offer. The recent A$550 million bond issuance by the BBB rated and NZ government majority owned Air New Zealand is one example. The 4 & 7-year bonds priced at a ~5.7% and 6.6% yield respectively, with the credit margin on the 7-year securities set at exactly 3% over the swap rate.

Albeit a smaller deal, the recent issuance of higher yielding Tier 1 capital notes from BBB rated P&N Bank also represented excellent risk-adjusted returns. Priced at 5.75% over a rising cash rate (i.e. returns that will increase with a higher RBA Cash Rate), these securities provide more than ample compensation for the subordinated BB- rated Tier 1 securities which are secured by ~14% in equity capital. We regard this as more than sufficient to weather any plausible downturn on its housing loans exposure.

Likewise, as highlighted in Chart 2, attractive credit margins of ~2% coupled with expected new supply in coming months makes BBB+ rated major bank Tier 2 securities a standout for most higher yielding credit portfolios.

Much of our conviction for Australian IG credit is predicated on the current health of mainstream corporate Australia, with financial leverage as measured by net debt to EBITDA currently at its equal lowest point for ~20 years (refer Chart 3). Along with having a proven ability to access new public equity to delever balance sheets when required, the current low leverage of corporate Australia provides a significant buffer to coming headwinds (i.e. a slowing economy from higher input costs and rising interest rates).

By contrast, the same cannot currently be said for some segments of the Australian credit market. In particular we are cautious on the levered loan space, where it seems significant inflows of new money from institutional and retail clients chasing a relatively smaller pool of assets (~$10bn p.a. of issuance) is driving poorer risk adjusted return outcomes. From our observations, while valuations have cheapened up significantly in publicly traded credit and look increasingly attractive, they have barely moved in the levered loan segment of the market.

While confidentiality agreements preclude disclosure of specific deals, we can provide some broad assessments of risk and return in this part of the market. For instance, levered names generally carry much higher risk, with credit ratings in the segment averaging ~B+ which is several notches below investment grade (which requires a minimum BBB- credit rating). With typical terms of between 5-7 years, these loans are still being largely issued at unchanged credit margins of between 350-400bps; in our assessment these offer poor risk-adjusted returns compared to public markets.

Moreover, the higher risk in the segment is largely predicated on much greater debt usage with leverage multiples (debt to EBITDA) averaging between 4-5 times, significantly higher than the current 1-times for mainstream corporate Australia. This higher debt burden can become problematic, with interest rates normalising over the next 12-18 months set to increase interest costs and potentially depress earnings in line with moderating economic growth.

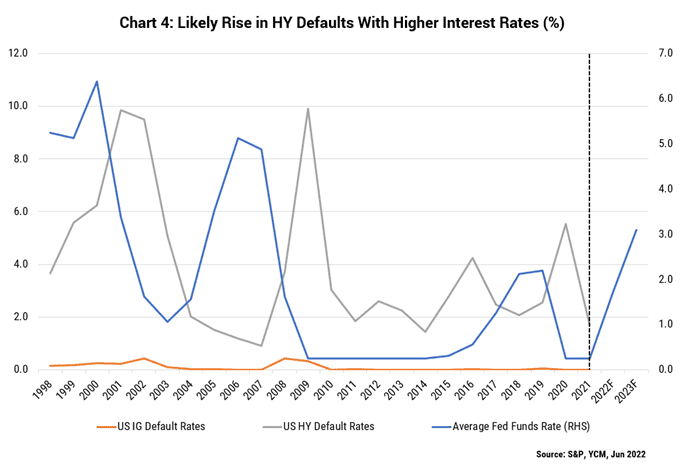

This combination of higher inflation, increasing interest rates and shrinking central bank balance sheets is likely to increase asset impairment risk in high yielding segments of the market such as levered loans. In the US, previous peaks in HY defaults have followed the peak in interest rates by ~12 months. By contrast, IG defaults are virtually non-existent according to S&P data (refer Chart 4). Given the projected increases in interest rates by central banks, it’s likely that high yield defaults will rise from 2022, especially after a prolonged period of lower-than-average defaults due to uber accommodative monetary policy.

So why does demand for levered loans currently remain so strong that valuations remain unchanged? Having access to this segment – and thus running the ruler over most of these deals – along with the best of the publicly traded space, we observe that while some levered loan deals continue to appeal, there are fewer in the current stage of the cycle which stack up on a relative value basis across the entirety of Australian credit.

Tracing the origins of the appeal of levered loans and other private debt style securities typically focuses on its track record post GFC, with strong returns and minimal impairments that have been underpinned by more than a decade of quantitative easing. Clients have generally been attracted to its higher credit returns, but also its low volatility on account of most private style debt portfolios being hold to maturity and not mark-to-market like publicly traded credit securities. This has appeal for institutional and retail clients for various reasons, and while this strategy has worked effectively for over a decade, the segment’s primacy over publicly traded credit – particularly investment grade – might soon be ending.

As we move into this new environment of higher inflation and interest rates, we expect investment grade credit’s risk-adjusted returns to increasingly outperform private debt. At current valuations, investors should be cognisant of the rising opportunity cost of remaining underweight. Moreover, private debt’s low volatility and hold to maturity status in a rising interest rate environment could be camouflaging rising impairments which are obviously not priced into current valuations.

In being truly multi-sector and operating across all sleeves of Australian credit, our Higher Income and Enhanced Income portfolios remain agnostic on where to source higher risk-adjusted returns, with a current bias to investment grade over high yield. The portfolios are generating ~5.8% and 5.4% yields* respectively from their high-quality average investment grade portfolios. Moreover, their floating rate running yields of ~3.8% and 3.1%* will also naturally increase with the cash rate and continue to provide interest rate duration risk protection.

0 Comments