For Phil Strano, Portfolio Manager of the Yarra Absolute Credit Fund, understanding a security’s structure is paramount to value assessment and a robust investment process. In this update, Phil looks at how investor opinion can vary when it comes to delineating between holding vs. operating company issuance.

Robust primary corporate issuance in the Australian MTN (AMTN) market has been a key feature of 2021, with a bumper $6.3bn of bonds/notes issued in the five months to the end of May, across REITs, Infrastructure, Utility and Industrial issuers.

Judging by their strong performance in secondary markets, most of these deals were priced attractively (or at least fairly), though opinions vary on the overall attractiveness of some of these primary issues and the perceptions of risk and adequate returns.

Two deals thus far in 2021 have been especially noteworthy in illustrating just how widely investor opinion and pricing can vary in a marketplace, and how perceptions of risk and value can splinter when issuing out of Holding Company (HoldCo) vs. Operating Company (OpCo) corporate structures.

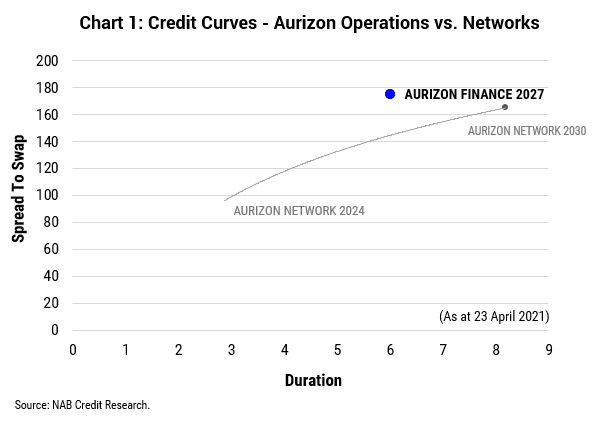

Firstly, let’s look at the Aurizon Operations (AZJ) 7-year $500m bonds issued in early March at a credit margin of 175 bps. Having established a new corporate structure in 2018, AZJ’s holding company now issues debt from its OpCos separately: firstly its Networks (below rail), and secondly its Operations (above rail). We internally rate each OpCo at BBB, or one notch below Moody’s at Baa1.

Despite Networks and Operations having identical credit ratings, the inaugural AZJ Operations 7-year bond priced at an attractively wide spread premium (+50 bps) to its sibling AZJ Networks (refer Chart 1).

In our opinion, while a spread premia of sorts was justified given Operations is more industrial like (i.e. backed by rolling stock assets) and Networks is instead more infrastructure like (rail track and associated assets), a 50 bps spread differential appeared very generous. Both OpCos have optimized debt levels to maintain strong investment grade credit ratings and share the same parent, business mix and destiny.

Now, let’s look at the Charter Hall Group’s (CHC) inaugural $250m 10-year bond issued in April at a credit margin of 140 bps vs. the existing Charter Hall Long WALE REIT 2031 bonds (CLW). In this instance, the CHC bonds were issued out of the HoldCo and backed by minority equity stakes (generally less than 15%) and the CLW bonds were issued out of the OpCo.

As with the Aurizon notes deal, both CHC and CLW issuers have identical internal and external investment grade credit ratings, BBB+ and Baa1 (Moody’s) respectively. However, unlike AZJ, the distinctions in the risk profiles of the two securities, in our opinion, were not adequately priced in, with the spread premium for the CHC bonds over the CLW bonds a modest 15 bps (refer Chart 2).

Moreover, the recent merger between the $5bn AMP Capital Diversified Property Fund and a Dexus wholesale fund provides an example of why the underlying risks associated with CHC’s HoldCo debt issuance should be adequately priced. In these cases, management fee revenue can be transferred by investors from the HoldCo to a new manager with little or potentially no compensation.

While Charter Hall’s hold on its assets is not under any near-term threat, we do believe their lack of direct ownership control over their OpCos needs to be factored into any assessment of value. For the April bond issue we did not believe it to be adequately priced.

The Yarra Absolute Credit Fund’s strict focus on maximizing risk-adjusted returns led us to participate in AZJ’s bond issue in March and decline CHC’s April offer. The Fund, which pays distributions monthly, has an average investment grade credit rating, has delivered an 8.2% return (net of fees) over the past 12 months and currently offers a running yield of 3.77% p.a[1].

0 Comments