Phil Strano, Portfolio Manager of the Yarra Absolute Credit Strategy, details why SEEK’s recent debt issuance offered investors a compelling risk-reward opportunity.

Debt issuance from Australian corporates has been running hot in recent months, with some $5.5bn of credit issued into the public and private markets since September 2019.

Hot on the heels of the $300mn David Jones Notes issue, online recruitment and education provider Seek (SEK) last week successfully issued a $150mn sub debt deal in the Australian market. Priced at an attractive initial credit margin of BBSW+370bps, the 6.5-year non-call 3.5-year (6.5nc3.5) notes provide further evidence of the high risk-adjusted returns on offer in public AUD domestic deals.

Key terms of the SEK deal include:

- Step-ups in credit margin if not redeemed at the 3.5-year call date (+200bps) or on a change of control (CoC) (min. 370bps ) respectively; and

- A shareholder dividend stopper effective should cumulative distributions on the notes not be paid in full in any particular period.

Our internal senior unsecured credit rating for the SEK deal is investment grade, with a two notch downgrade applied for the issue’s subordination giving it a lower rank in the capital structure. We value the issue as a shorter dated 3.5-year deal – the key terms financially penalise SEK if it extends beyond 3.5-years – which at +370bps looks attractively priced compared to the publicly traded BB universe (refer Chart 1).

More broadly, our positive view is also supported by SEK’s dominant market position – the ~$8bn company is the Australian leader, with a 20+ year track record, an increasingly diversified earnings stream and strong balance sheet.

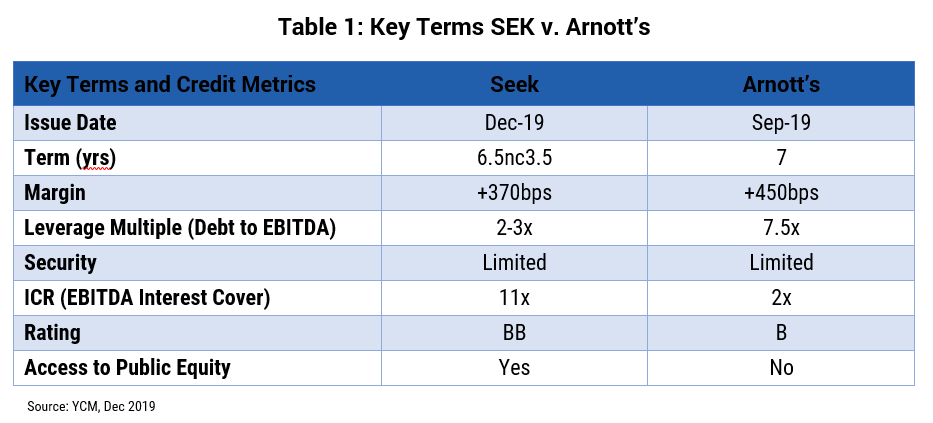

The SEK deal is also attractive when looking across the spectrum of recent Australian private debt/levered loan deals. In particular, comparing SEK’s public note with KKR’s recent private deal to fund the acquisition of Arnott’s (refer Table 1) provides an interesting contrast.

On risk-adjusted terms, the SEK offer (3.5-year, ‘BB’ rated, BBSW+370bps) looks far more attractive than the Arnott’s deal (BBSW+450bps, 7-year, ‘B’ rated): (i) SEK has a much stronger credit profile (lower leverage and higher interest cover); (ii) it offers a significantly shorter effective maturity date; and (iii) permits the raising of public equity capital to de-lever in more difficult trading environments (if required).

While pricing in Australian ‘hold-to-maturity’ debt remains attractive, there are still compelling opportunities to be identified in the public market. Yarra Capital manages credit and liquidity risk for clients by identifying the most attractive risk-adjusted returns across ALL public and private debt sleeves of the Australian Credit market to build diversified, flexible portfolios.

0 Comments