The Reserve Bank of Australia (RBA) has announced the biggest change to the monetary regime since 1993. A change announced without notice, without debate, and without supporting research. For Tim Toohey, Head of Macro and Strategy at Yarra Capital Management, it raises more questions than it answers.

If you were tasked with fundamentally changing the operating target for monetary policy in a major developed nation how would you go about it?

The Federal Reserve has just completed 18 months of community consultations, detailed research papers, dedicated multi-day conferences and numerous speeches by the Fed Chairman, the Vice-Chair and the various FOMC members on the potential shift to ‘average inflation targeting’ before implementing it as policy. It has been a thorough, if not exhaustive, approach to discuss the various options, engage with stakeholders and inform the public that a significant change is coming. In the end, the Fed’s version of average inflation targeting, without a symmetric catch-up following any period of inflation undershooting, is not too different from what the RBA currently practices. Or at least so we thought.

In Australia it appears we like to do our monetary policy regime changes differently. Yesterday the biggest change in the monetary regime since Australia first adopted inflation targeting in 1993 was added at the backend of a speech at an investment bank conference on a topic billed as a discussion on the uneven nature of the economic recovery. The title of the speech did not hint at the seismic shift in policy the RBA was contemplating. There were no detailed research papers released beforehand, no reference to a looming change in the official communication channels of the monthly RBA meeting, the more detailed Minutes of the meeting or the Statement of Monetary Policy. There has been no opportunity to discuss the proposal in an open forum or any attempt at broad-based consultation.

Instead, in the space of a few sentences, the RBA swiftly cut ties with forward-looking pre-emptive inflation targeting – arguably the most successful and consistently applied policy framework in the developed world – in preference to a regime where monetary policy will now be calibrated on the basis of where inflation has been rather than where it is going.

The change raises far more questions than the RBA has provided answers.

What is the motivation for the change?

Is it that the RBA no longer believes in its own ability to forecast inflation?

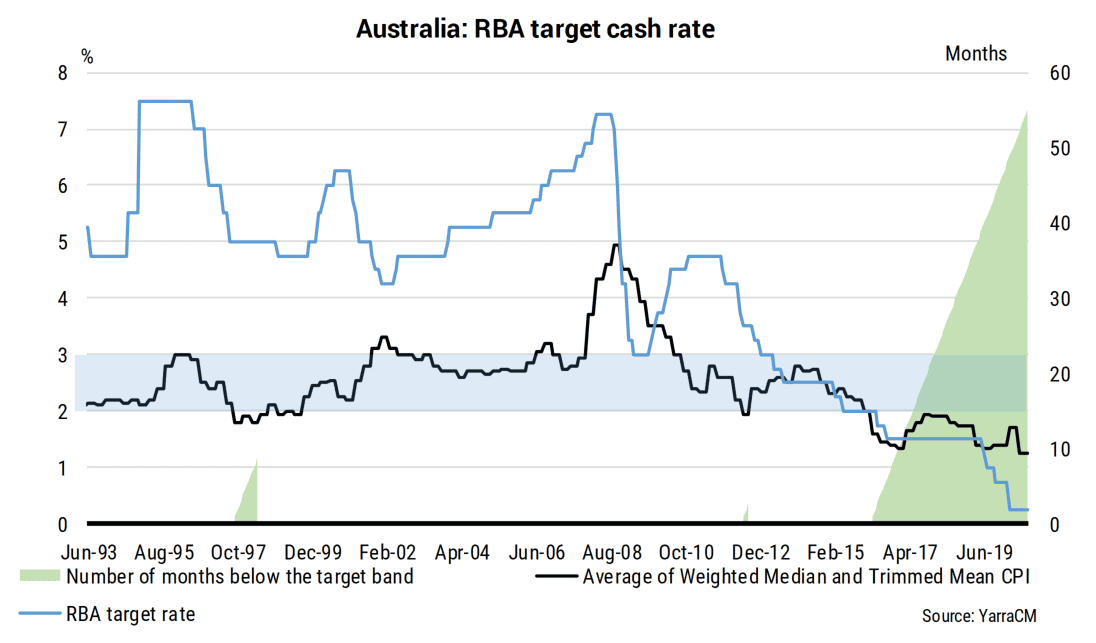

It has now been 71 months since underlying inflation was at the mid-point of the RBA’s target band of 2-3% and 56 months since inflation was at the bottom of the band. Both are record misses for the RBA during the inflation targeting era, and as a consequence there has been a persistent pattern of the RBA revising down its forecasts for inflation over the past six years. However, it appears the RBA response has not been to double its research efforts to inform its understanding of current dynamics on inflation. It seems it merely conceded that the easiest path is simply target historical inflation. Obviously, the RBA will still talk about inflation and where it might be going, but that is very different from actively managing policy to achieve a specific forecast for inflation.

Is it that the RBA believes their remaining policy options are so powerless that they cannot generate sufficient aggregate demand growth to influence inflation?

That is, is the RBA conceding they no longer have the policy bandwidth to generate a desired inflation rate? It was not long ago that the RBA was openly dismissive of other central banks attempts at quantitative easing (QE), particularly cutting near the zero bound and quantitative QE policies. However, the RBA has rapidly shifted the goal posts to embrace both yield curve targeting and now, it seems, a shift towards the more common quantity targeting based version of QE.

Is it because the RBA no longer believes in the concept of NAIRU?

It was notable in the Governor’s speech that the RBA clearly wants unemployment lower, but how low are they actually targeting for the unemployment rate? Prior RBA research clearly shows that inflation is generated via wage inflation if the unemployment rate is below the non-accelerating inflation rate of unemployment (NAIRU) and also the pace that the unemployment rate falls towards the NAIRU. The has now RBA declared that they simply won’t respond to a falling unemployment rate. It is no longer a sufficient condition to commence the discussion over changing the path of interest rates. Whether this is merely an acknowledgement that they have no idea where the NAIRU is in real time or whether it is a full repudiation of the Phillips Curve is an important open question.

Is this change to a backward looking inflation targeting regime a temporary change, likely to change back to the old regime in a post-COVID, post vaccine world?

Is this now the new permanent regime likely to last the next 20 years? Or is a transitional arrangement on a path to a new framework?

So what could be some of the implications of the RBA’s unexpected change in policy regime?

The single biggest asset any central bank has is not on its balance sheet and it is not its ability to change reference interest rates. It is its ability to influence inflation expectations across the economy.

The RBA has the best resourced economics research department in the country with a long tradition of analysing and forecasting inflation trends. They may not always get it right, but on average they get it right more often than anyone else. Their forecasts are used as a guide for unions and employers negotiating wage agreements, companies in setting their pricing plans, and of course financial markets. Non-RBA economic forecasters are greatly influenced by the RBA’s inflation forecasts, perhaps more than the RBA realises. However, shifting to a regime where the path of inflation is no longer at the heart of the RBA’s research efforts, even if it still produces inflation forecasts, makes everyone less informed. The RBA’s role in shaping inflation expectations may simply diminish over time as the market realises the RBA is merely looking backwards.

The concepts of forward looking inflation targeting, NAIRU, the Phillips Curve and market determined bond yields are the bedrock of the vast majority of the RBA’s economic models, including the relatively new Martin model.

However, what use are the historical models which are based on economic concepts that RBA Board are no longer using to determine policy upon? Do the models need to be rebuilt? If so, what is the RBA using for its deliberations in the interim?

The announcement that the RBA is now thinking of buying bonds beyond the 3-year point of the curve was another stunning announcement from the speech. It was only 28 days ago that the Deputy Governor gave a comprehensive set of reasons for why they won’t buy bonds beyond the 3-year point.

It is not clear what has prompted such a sharp backflip in such a short time. The RBA did offer that a reason for considering buying 10-year bonds is that Australian 10-year bonds are higher than some other countries. We may be old-fashioned but different financial prices for sovereign bonds tend to be associated with different views on the relative outlook for that economy, even in the presence of QE. A slightly more optimistic view on Australia’s economic prospects can easily be made vis-à-vis the rest of the G7 currently, and it’s hardly surprising that Australian 10-year yields are slightly higher. It is questionable what economic service is being provided to artificially bring Australian 10-year bond yields in alignment to foreign bond yields despite very real differences in economic fundamentals. Moreover, what happens when larger countries alter their long dated bond buying and global yields change? Does the RBA fight the move, move in tandem, or stand still? What will be the impact on market liquidity of sovereign bonds if the RBA merely compresses yields to align with global peers? What will be the implications for market participants who seek to hedge their exposures via global interest rate differentials? What will it mean for attracting global capital? None of these issues are likely to be enhanced by the RBA’s and none of these questions were addressed in the RBA’s speech.

In a similar vein, one of the most notable shifts detected in the speech was centred on the exchange rate.

Overtly targeting the exchange rate is a red line that the RBA has been careful not to cross over many years. However, this red line has now been tentatively crossed. Specifically, Governor Lowe stated:

“Australia is a mid-sized open economy in an interconnected world, so what happens abroad has an impact here on both our exchange rate and our yield curve. In the past, the interest differentials provided a reasonable gauge to the relative stance of monetary policy across countries. Today, things are not so straightforward, with monetary policy also working through balance sheet expansion. As I noted earlier, our balance sheet has increased considerably since March, but larger increases have occurred in other countries.”

The inference is the RBA is considering weaponising QE to generate a lower exchange rate. The linking of relative bond yields, the exchange rate and relative QE by the RBA Governor is no accident. However, for a central bank that rarely seeks to influence the $A, flagging a willingness to engage in competitive depreciations via QE is truly a big shift.

Perhaps some of these questions will be addressed in the November Statement of Monetary Policy. However, if this speech is a guide it might just open up more questions than answers. Indeed, explaining the rationale for a likely 15bps cut in the cash rate at the November meeting in the Statement of Monetary Policy is now the least of the RBA’s issues.

0 Comments