In this latest Australian Equities Insight, Dion Hershan, Head of Australian Equities, looks at some examples of inflation observed through the early part of the Australian company reporting season.

Anyone feeling sceptical about inflation would be wise to tune in to the final week of the August reporting season. If the first three weeks are any guide, inflation is no longer on the horizon. It’s here.

It was easy to dismiss inflation as being ‘transitory’ when it appeared in a select few items (lumber, airfreight), but company results confirm just how far-reaching it appears to have become. This has significant implications for rates and the margins of public companies. As one company reprices to recover input cost inflation, it can become self-perpetuating.

To share a few anecdotes:

- Mining costs

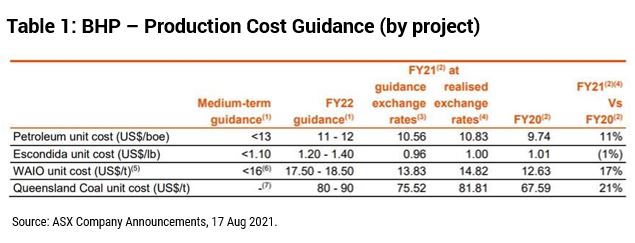

BHP, best-in-class in cost containment, cited production costs would be going up by 17% in iron ore, 21% in coal and 11% in oil (refer Table 1);

- Construction costs

Cost blow outs have been reported so far by Bluescope Steel (+5-10% to accelerate its North Star expansion), Mineral Resources (+24% across its business) and Oz Minerals (+13% relating to growth capex);

- Cost recoveries

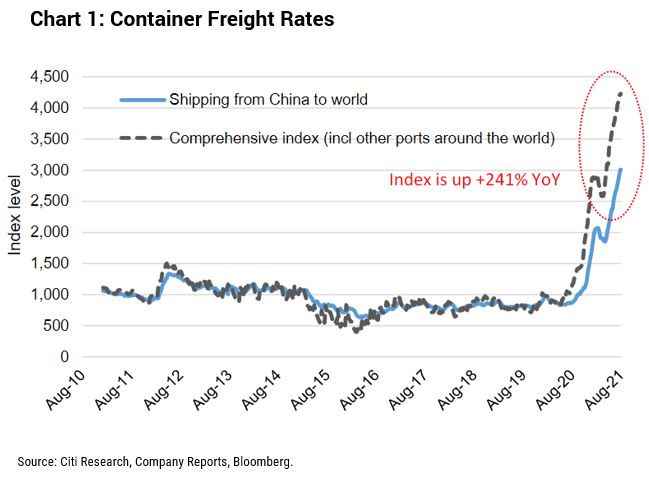

Amcor cited price rises of around +5% by the start of FY22 in an attempt to recover rising input costs from raw materials (resin, aluminium and titanium dioxide), while Brambles made similar comments to recover lumber costs. Rising prices y/y for steel +317% [1], oil +52%, and freight +241% (refer Chart 1) are a recurring theme and companies are vigilantly trying to pass through costs to consumers;

- Insurance prices

Surging pricing evidenced by premium rate rises. QBE delivered +10%, SUN passed through +7% in Home and +6% in Motor, and IAG announced +8%;

- Tightening labour

SEEK’s job ads index was up +91% in June (y/y) (pre Syd lockdown) after hitting a record high in March, tightening labour markets are driving spot surges in wages in niche areas, in part due to a lack of immigration and border restrictions. Labour shortages were a theme across a number of results, including Domino’s Pizza, Downer EDI, Brambles, ARB Corporation, BHP Group and CBA (referring to Construction). Even CSL saw blood collection costs skyrocket by over 30%, with rising employment and lingering COVID hesitancy forcing it to move its donor incentive fees higher.

Although COVID and lockdowns (quite rightly) dominate headlines and short-term thinking, inflation and the consequent margin pressure it can create will be an important issue in the years ahead. Our strong sense is most investors are either complacent or dismissive of the issue, and only when they start to see margins and earnings decline will the issue come into sharper focus.

The issue only reinforces our preference to skew our portfolios towards high quality companies, in attractive industry structures with strong pricing power such as Ansell, James Hardie, Aristocrat and ResMed.

0 Comments