While maintaining blind optimism as an investor often seems a lot easier and is probably more fun, it’s worth keeping in mind that rewards instead tend to come over the long term by being realistic.

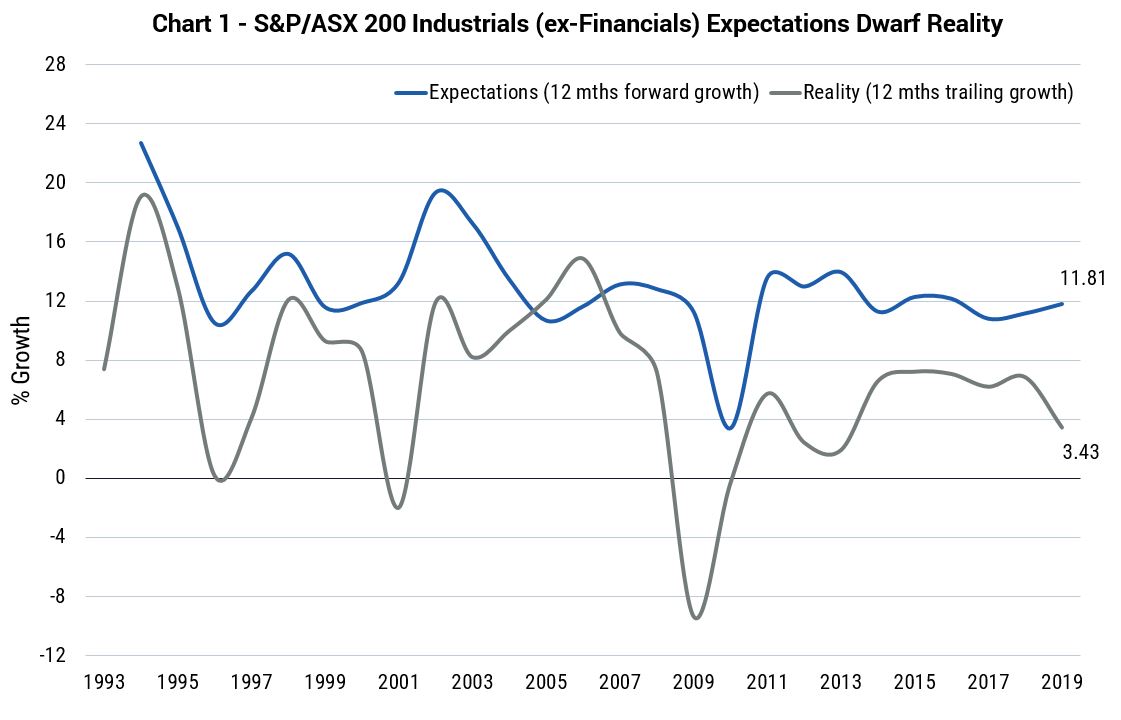

Looking today at the Australian Industrials sector (40% of the ASX 200 by market cap), expectations appear well suited to ‘fairy tale’ investing, notwithstanding 13 consecutive years of consensus downgrades and the sector’s low single-digit growth for the past decade. In fact, despite expectations of double-digit growth in each of the last eight years – which has been delivered in precisely none of them (refer Chart 1) – the proverbial hockey-stick is back once again for FY20.

Source: Credit Suisse, IBES consensus estimates.

As reporting season nears, it is bizarre to note that FY20 Industrials earnings are now forecast to grow by ~10% even though consensus downgrades have averaged 5% over the last five years. In our opinion that could well be a reasonable proxy for the year ahead.

Focusing on the macro, the Australian economy (and the global economy more broadly) is currently in a grind, with interest rates low and going lower for a reason. Stimulus (monetary and fiscal) is a response to the environment, not a catalyst for improvement.

In our view, disappointment could come at exactly the point that valuations are stretched. The Industrial sector is now trading 2.5x standard deviations away from the long term average, at 22x P/E, an earnings number that could prove too high (refer Chart 2).

Source: YCM, FactSet consensus estimates, Industrials excluding Transportation & Infrastructure, 26 July 2019.

At Yarra, we maintain a rational and disciplined approach when valuing companies. To that end we are underweight Industrials, in particular the higher growth/higher valuation companies. Within the Industrials sector, we are invested in a number of those less ‘exciting’ businesses (where the market has low expectations) with attractive valuations, including Incitec Pivot, Worley, Downer EDI and Nine Entertainment.

0 Comments