Katie Hudson, Head of Australian Equities Research and Small Cap Portfolio Manager, looks the August reporting season in the small cap equities space, where the market environment is creating significant opportunities both in terms of what to own and what to avoid.

Against the backdrop of a recession, the highest unemployment in 22 years and talk of a fiscal cliff it was fascinating to see the consumer discretionary sector (largely retailers) outperform so strongly during the August 2020 reporting season, up 22% in the month [1] alone.

The combination of pent-up demand in most states post the lockdown, higher discretionary income for those with jobs (i.e. due to lower travel, car parking, entertainment and childcare costs) and money flowing from JobKeeper and superannuation withdrawals combined to give the listed retailers a massive sales boost during the important July trading update window.

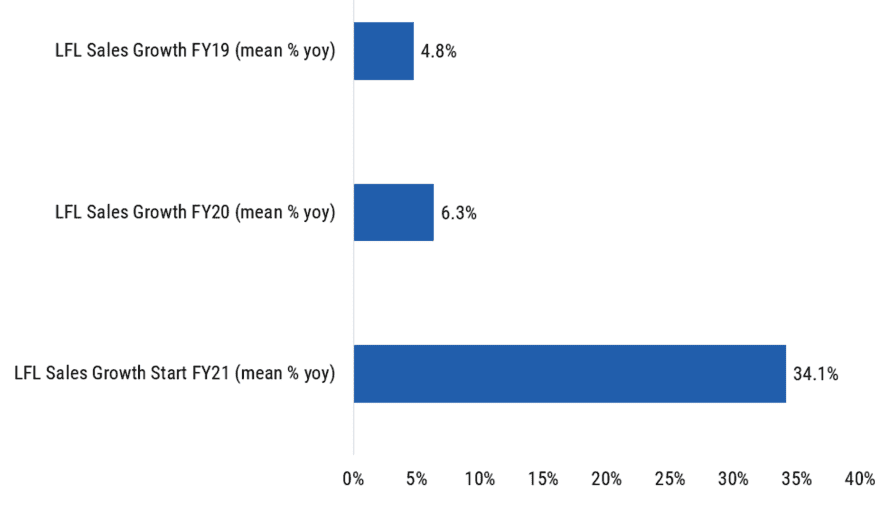

The chart below highlights the shift. Listed retailers, which had been struggling to generate sales growth above 4-5% over the last few years, reported an average of 34% like-for-like sales growth in their trading updates.

Chart 1 – Australian Discretionary Retail Like-For-Like Sales [2]

On the back of these strong early sales trends, analysts have upgraded their forecasts and now expect 29% net profit growth in FY21. This upgrade momentum saw investors re-rate the share price multiples for retailers by 26%, with share prices now trading above pre-COVID levels in many cases.

There are two reasons why we think the listed retailers have outperformed their unlisted retail peers, one structural and one temporary.

First, the acceleration in online sales drove a shift towards those larger retailers with a stronger online capability, a trend we believe will persist.

Less likely to persist, in our view, is the transfer of spending to the furniture, homewares and hardware categories such as that experienced by the likes of Adairs, Bunnings, Harvey Norman, JB Hi-Fi and Nick Scali.

When undertaking research to understand volatility in operating trends, earnings forecasts and share prices, we are often asked how we are navigating these markets. The key question for us hasn’t changed: has the long term earnings power of this company or sector changed?

An acceleration in online sales makes a nice headline but there is little evidence that it is sustainably growing the profit pool for retailers. As government subsidies roll off and rent abatements cease, the benefit to retailer profits will become a headwind to earnings. And as consumers resume their normal activities the recent spending shifts are unlikely to persist.

The tendency for investors to extrapolate short-term trends has been on overdrive during the pandemic. This is only one example but there are many more.

For investors prepared to act with a long term mindset this market environment is creating significant opportunities both in terms of what to own and what to avoid.

0 Comments