Markets seem certain the US Federal Reserve (FED) is going to cut rates and almost as certain the Reserve Bank of Australia (RBA) cutting cycle is done and have started pricing in small hikes for 2026. While it’s not uncommon for either central bank to move at different times and even different directions, there are usually differences in the US and Australian economies that lead to these differences.

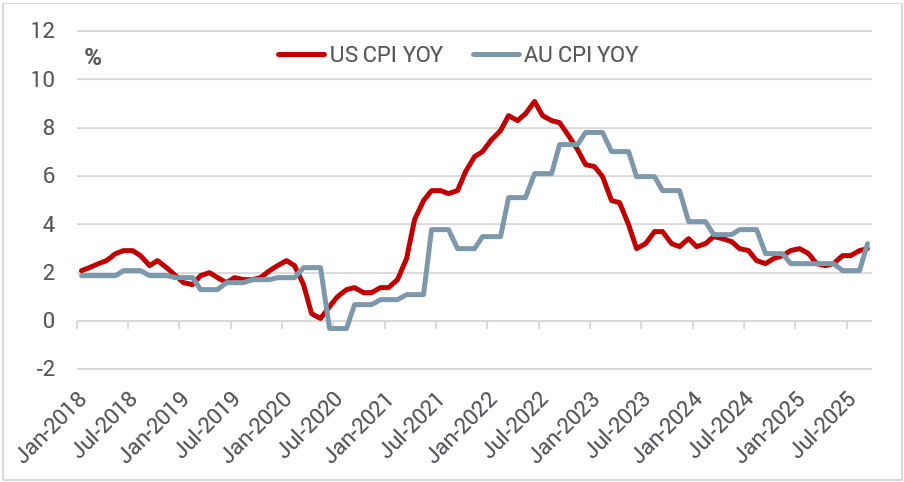

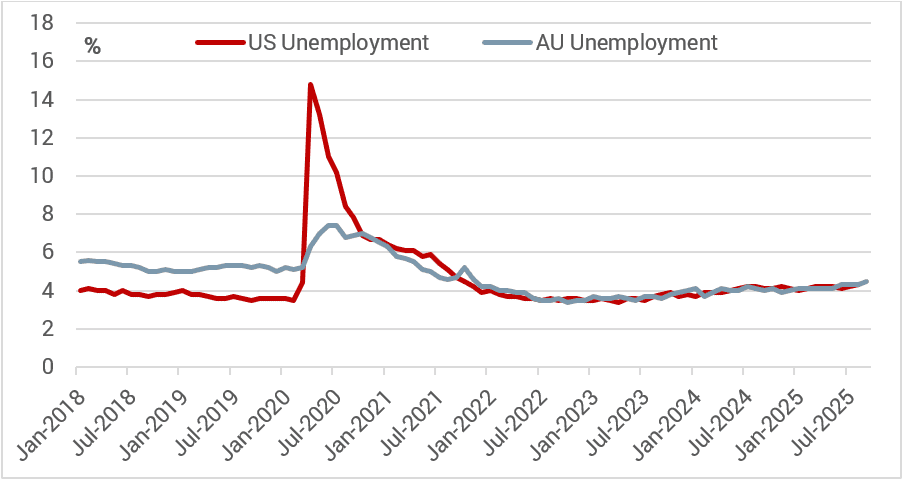

Looking at US and Australian CPI and Unemployment it’s difficult to see how we end up with such different views based on the data. Since 2018, both countries unemployment and inflation rates have been quite similar (refer Chart 1 and Chart 2).

Chart 1. AU v US CPI (YOY%)

Source: U.S. Bureau of Labor Statistics, Australian Bureau of Statistics.

Chart 2. AU v US Unemployment (%)

Source: U.S. Bureau of Labor Statistics, Australian Bureau of Statistics.

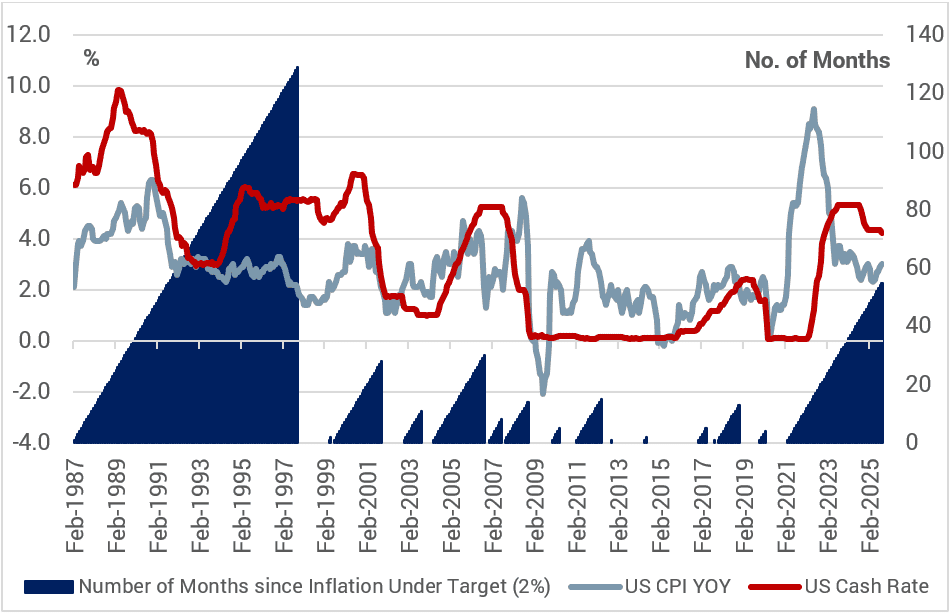

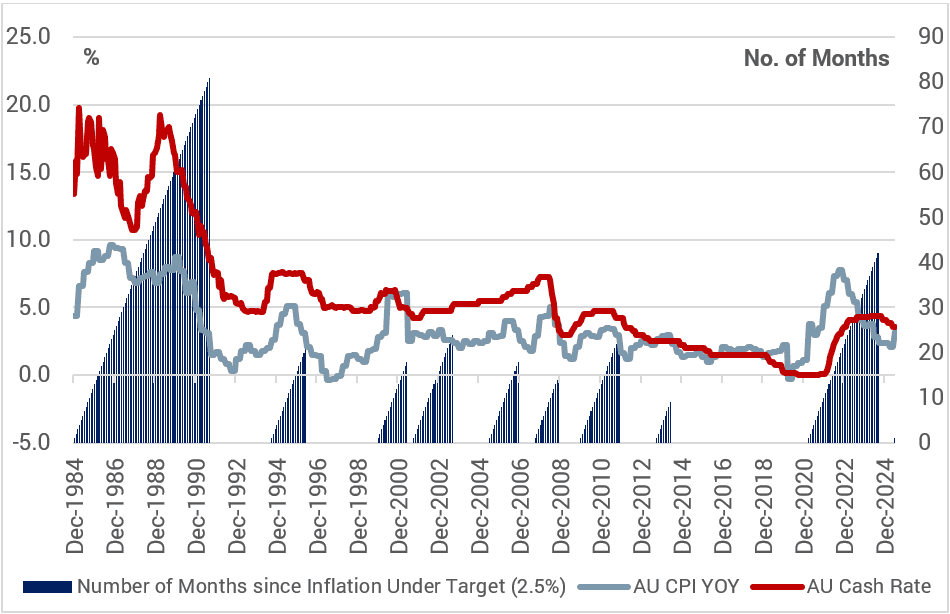

The RBA has also come under a lot of criticism for being behind the game from a lot of market commentators, but if we look at chart 3 and 4, the shaded area shows the number of months in each monetary policy cycle for the FED and RBA to bring inflation back to target. The RBA has managed that feat, admittedly briefly, however the FED after 55 months still has not gotten back to their inflation target (refer Chart 3 and Chart 4).

Chart 3. US Cash Rate and Inflation

Source: U.S. Bureau of Labor Statistics, U.S. Federal Reserve.

Chart 4. AU Cash Rate and Inflation

Source: Reserve Bank of Australia, Australian Bureau of Statistics.

While we think the RBA is probably on hold for a few months to mid-2026, we are hugely sceptical that the FED should be cutting rates as aggressively as the market is suggesting.

What does this mean for Fixed Income investors?

With the recent backup in Australian yields, Australian fixed income looks to be a considerably better place to invest than in the US.

0 Comments