When would be a good time not to hike rates? Perhaps, just perhaps it is when war with Iran, one of the largest and longest feared geopolitical risks, turns into a sudden reality. Perhaps, just perhaps it’s when one of the largest technological shocks in modern history, AI, suddenly threatens to unravel the structure of the labour market. Perhaps it’s when the one clearly identifiable financial stability risk, excess lending in private credit, threatens the closest thing to a deposit bank run for credit investors since the financial crisis. Surely, it wouldn’t be when all three events occur simultaneously.

‘Policy of least regret’ was a statement that we once believed was tattooed on RBA senior staff and RBA Board members upon admission. In a dynamic and highly fluid environment of multiple exogenous shocks the modus operandi of sensible policy making is to pause, collect all relevant data points, assess, scenario plan and then make a strategic forward-looking decision. It seems this is a very different RBA.

It is clear the RBA continues to believe that Australian economy is operating above its productive capacity, and it is clear they have conviction that excess domestic spending is behind much of the excess inflation prints in 2025. We have previously debated whether these strong conviction views from the RBA are indeed correct[1].

But we have now moved beyond this concern. We feared in February that the RBA had turned hawkish when the economic cycle had already peaked and financial conditions had already tightened. Today we are concerned that the RBA is tightening into a series of economic shocks that risk a far more material economic slowdown than Australia needs nor deserves.

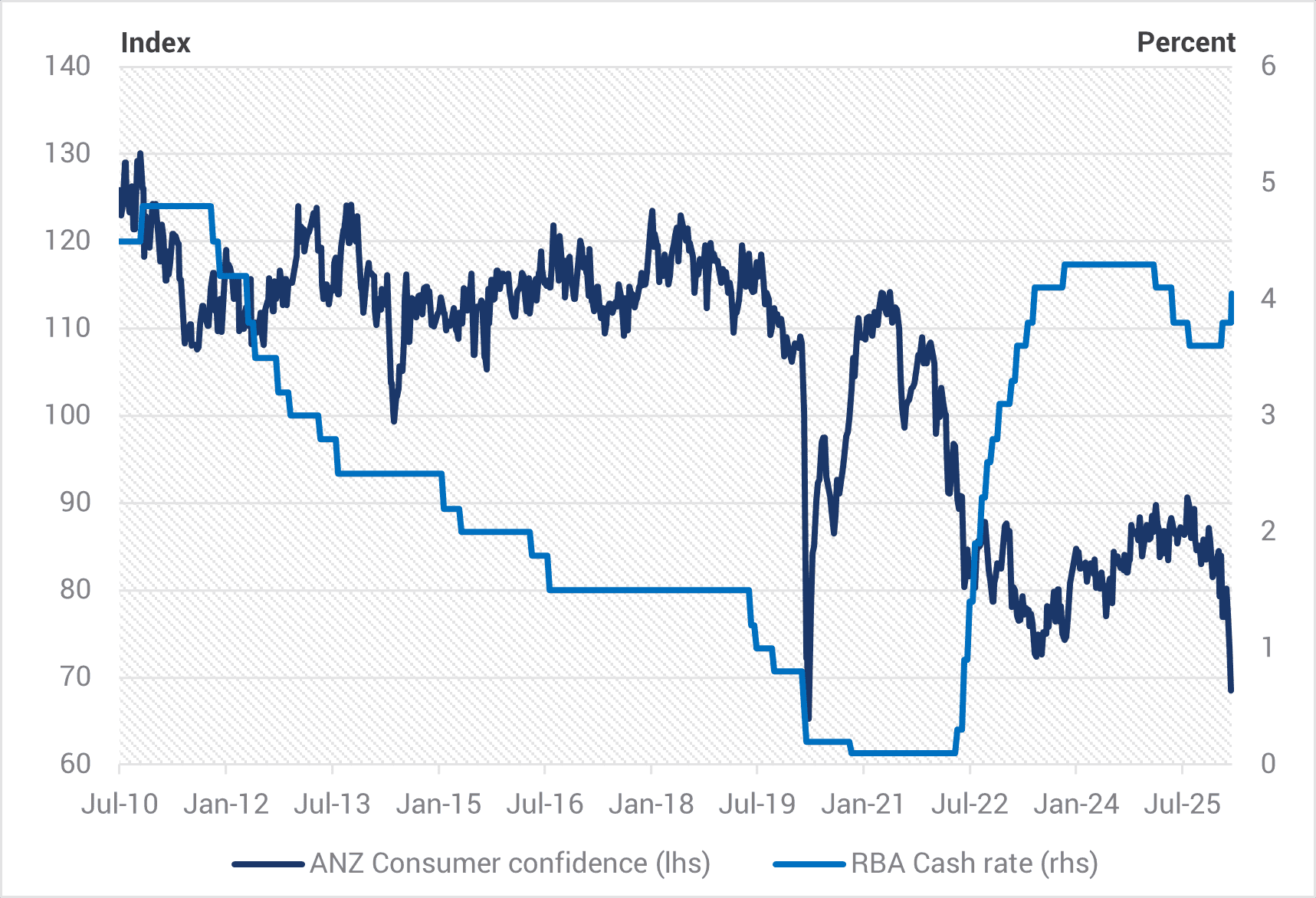

Let’s start with the obvious. A series of highly uncertain events tends to be highly corrosive to confidence. It is no surprise that the ANZ weekly consumer confidence indicator declined this past week due to events in the Middle East. Yet the decline in consumer confidence commenced in mid-2025 and this decline is now accelerating. We have just completed the largest three-week decline in the index since the abrupt collapse during COVID (Figure 1). While the solution to the COVID crisis was to cut interest rates precipitously and throw 10% of GDP of fiscal stimulus at the problem, our policy approach this time is to embark on a tightening cycle of 50bps, threaten more in the future and contend a period of fiscal austerity is urgently needed.

Figure 1. Consumer confidence and the RBA cash rate

Source: RBA, ANZ, March 2026.

This sharp decline in confidence, is not as the Governor today described as “having been low for a long time”. It is a dramatic fall that suggests a large air-pocket for discretionary spending is imminent. The impact of this expectations shock will be compounded by the failure to realise that the fundamentals that drove the consumer economic recovery in 2025 had already faded by calendar year-end.

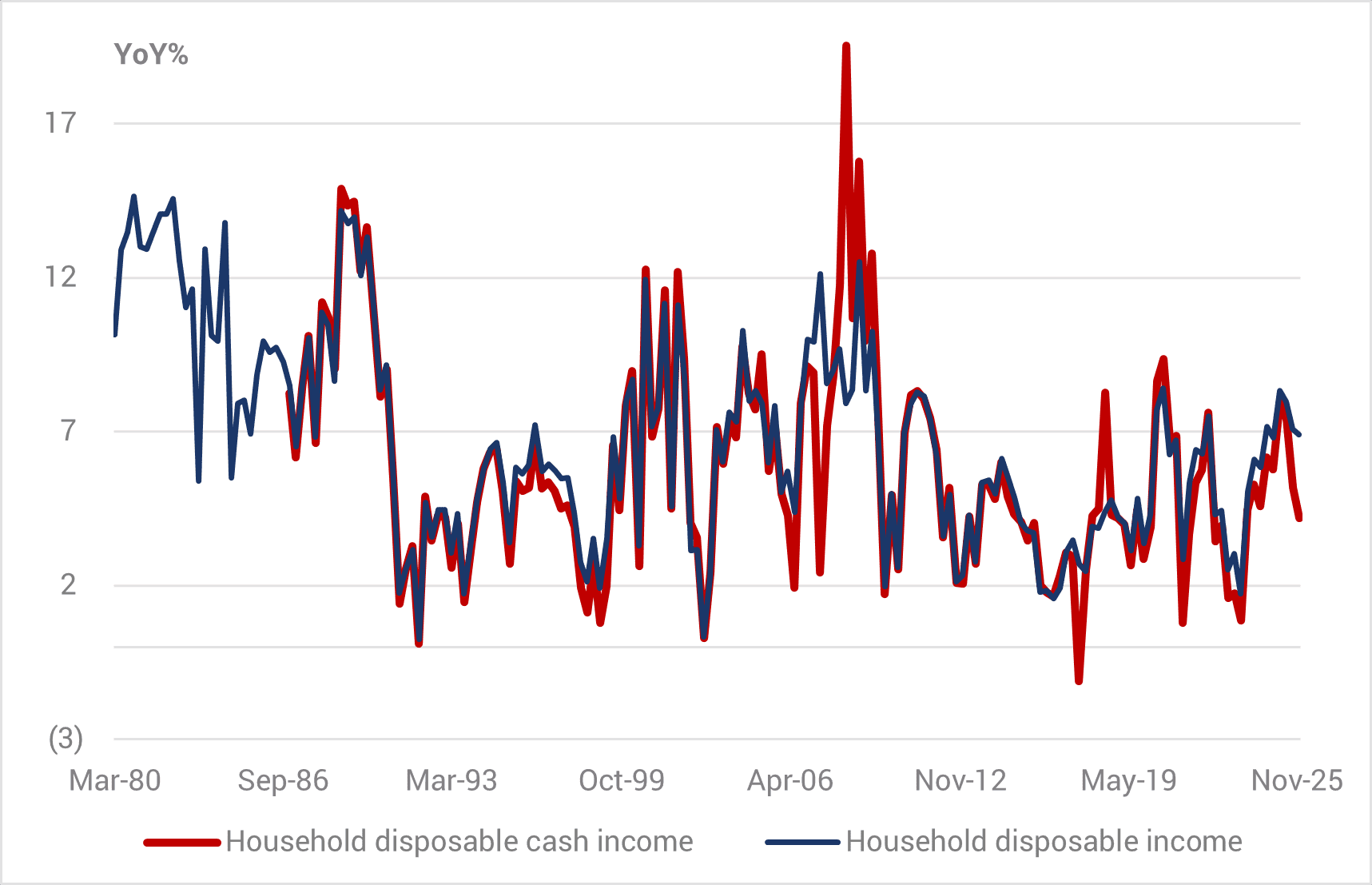

Many analysts point to the impact of the prior three rate cuts, income tax cuts and the wealth effect in driving the consumer recovery. All three assisted, but the core driving force was slowing ‘essential spending’ prices relative to sticky wage income growth. The result was a sharp rise in household cash income growth. But we are now well through the peak. Even before the year concluded, cash income growth for the consumer was slowing sharply.

Currently, we are in an environment of slowing wage income growth and sticky essential spending item prices (think rents, property rates and insurance). Even before the oil price shock, household cash income growth was eroding. Now with higher fuel and interest charges rising it is under siege (Figure 2).

Figure 2. Cash income had peaked prior to RBA hikes

Source: ABS, Yarra Capital Management, March 2026.

Yet the Iran War may not be the biggest threat that Australian policy makers should fear. We have all marvelled at the speed of development of the AI models and the spread of AI agents, yet for policy makers the threats or opportunities from AI were, not unreasonably, thought to reside beyond the policy setting horizon of the central bank. But clearly a lot has changed in 2026. Interestingly, in recent weeks it seemed the RBA was more concerned about the competition to resources that building data centres would have on inflation rather than presenting any coherent thought leadership on what the potential scenarios AI present for the Australian economy.

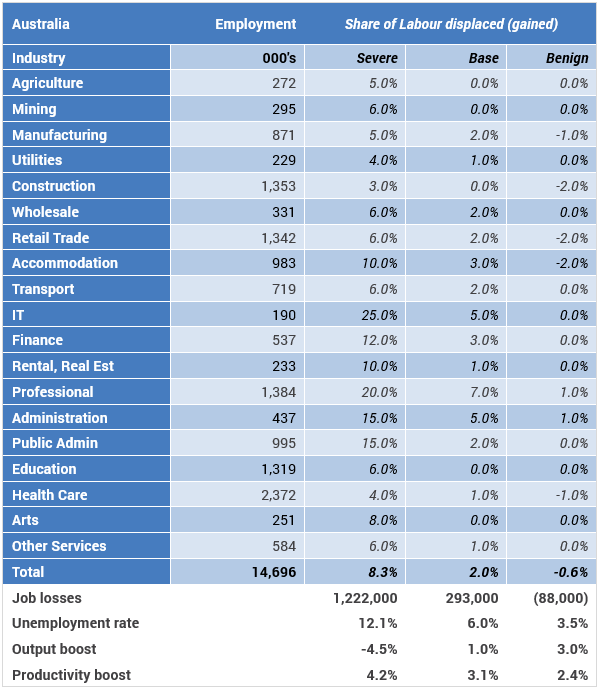

Even a back-of-the-envelope scenario analysis (see Table 1) where an assessment of the size of potential labour market displacement is assessed by industry and the implications for activity and productivity are calculated, albeit under broad rules of thumb, reveals that any scenario where higher interest rates are part of ‘the solution’ to the AI shock are difficult to envision..

Table 1. Scenario analysis: The impacts of AI on the labour market could be dire

Source: ABS, Yarra Capital Management, March 2026.

AI is now threatening a disinflationary shock of the highest order and crucially this is now plausibly set to occur within the next two years. It is no longer a nice-to-have ancillary to labour. It is now an unregulated and direct competitor with labour, with rapidly declining marginal cost and exponentially rising capability.

Frankly, one would have to be an eternal optimist to conclude the most likely outcome is the ‘benign’ scenario where AI grows the economic pie so much that the net employment impact is positive and the productivity boost is positive. But even under that scenario the ‘neutral rate of interest’ in Australia would be declining and raising interest rates would not be a fait accompli. It is hard to be prescriptive on outcomes at this early stage.

However, in thinking through the range of scenarios we believe that if AI is indeed deployed at scale in Australia over the next two years, our base case would be the unemployment rate closer to 6% than the current 4.1%, productivity would likely grow at double its long run average and wage and inflation outcomes would be printing well below the RBA’s targets. AI will more likely compound the next economic downturn since the first instinct of firms will be to seek to protect revenues via cost-out labour shedding strategies.

We are more focused on where the nature of the shock will directionally take the unemployment rate and wages rather than the RBA’s approach of focusing a wider array of indicators to tell us how the labour market is tracking relative to its recent historical trend. The debate whether job ads or the hiring rate of labour have really picked up very much into late 2025 and early 2026, has somewhat been rendered obsolete. Given the lagging nature of the labour market, a modest rise in job ads merely confirms the strength in activity growth in 2H25 and the seasonal optimism that attends the start of each calendar year.

However, we suggest it is difficult to contest the argument that there will be an extrapolation of those positive labour demand and activity trends in light of the developments of the past month. Time will tell, but we suspect history will show that the RBA just tightened policy ahead of renewed weakening for labour demand and amid the release a generational shift in productivity enhancing technology.

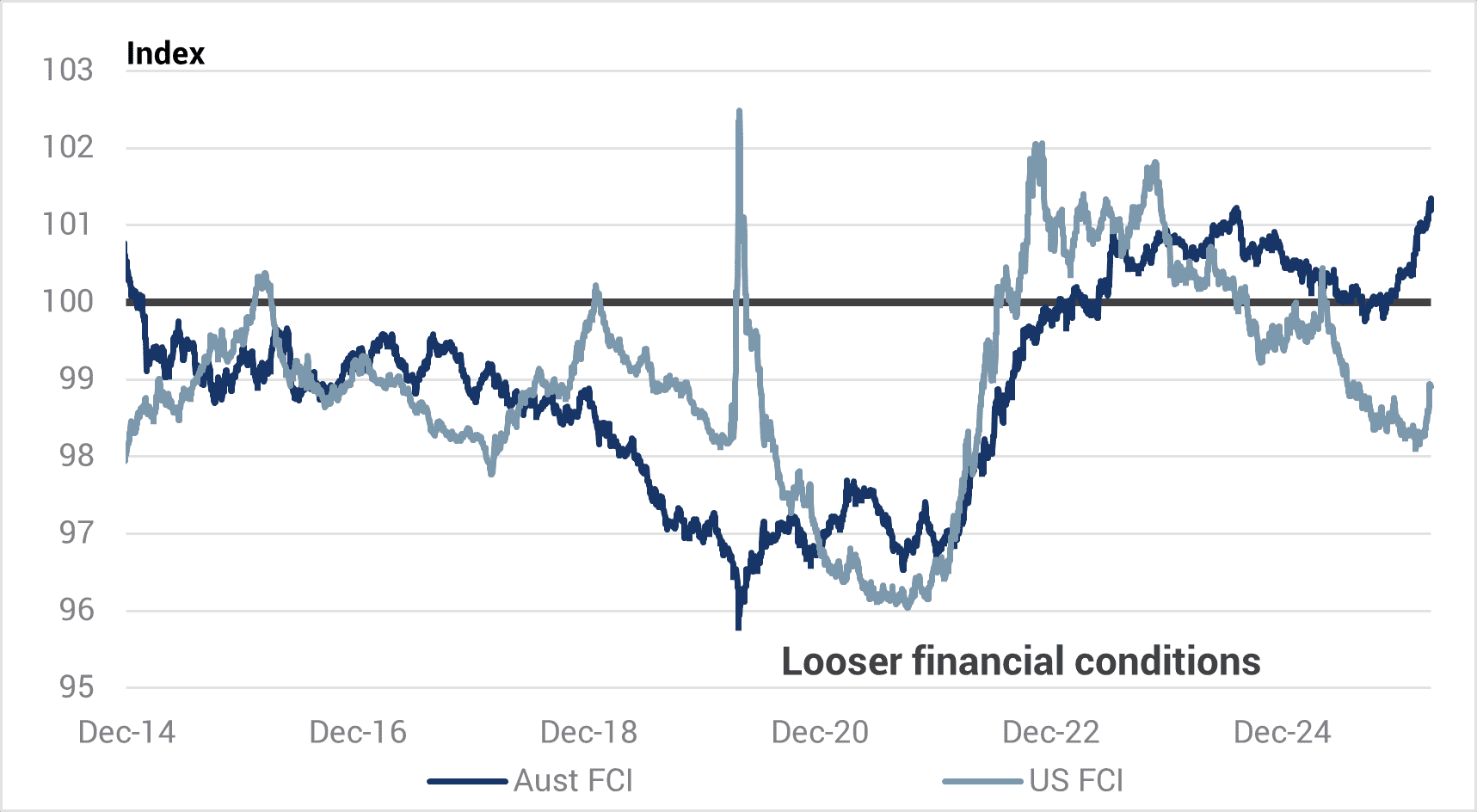

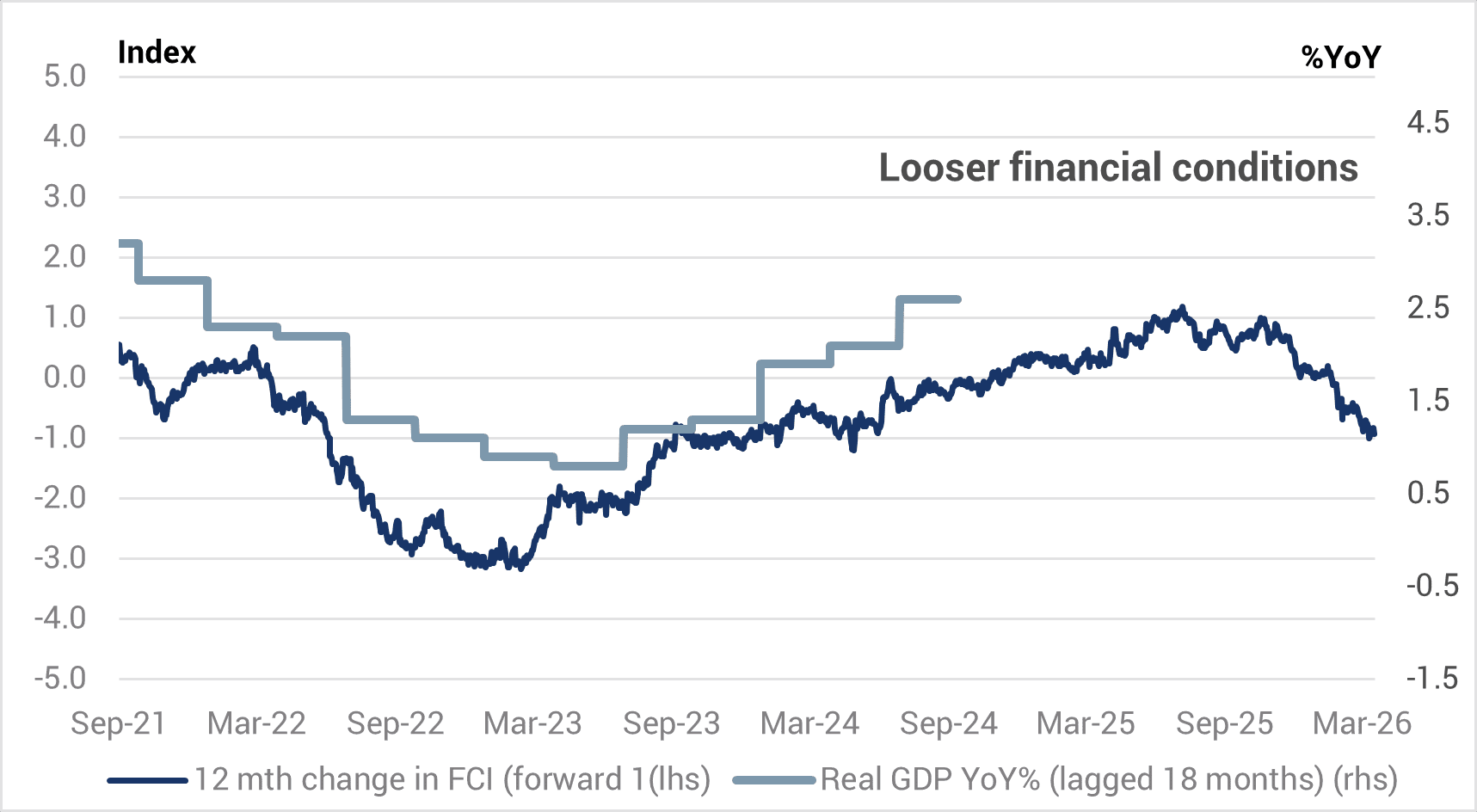

We also fundamentally disagree with the RBA over the appropriate way to measure movements in financial conditions. We have been making that case for several months that financial conditions had been tightening, principally because of a higher Australian dollar, but more recently due to higher bond yields, wider spreads and weaker equity markets. These latter forces are now also tightening financial conditions around the world, including in the USA (see Figure 3).

Figure 3. Australian and US financial conditions are tightening

Source: Yarra Capital Management, March 2026.

Figure 4. Financial conditions are consistent with economic growth slowing to ~1% pace in 12-18 months’ time

Source: Yarra Capital Management, March 2026.

We can reconstruct our financial conditions indices to include oil prices but this only strengthens the conclusion that financial markets have already tightened policy by more than enough to bring Australia’s economic growth to a sub-2% pace. Indeed, it is currently consistent with economic growth slowing to a 1% pace over the next 12-18 months. One can only imagine what will happen to financial conditions if private credit’s woes metastasize into a credit spread widening event. We have no idea how any central bank can be reassured that this is not a material near-term threat that should at least give pause for reflection and assessment.

Although we have been building and optimising financial condition indices for decades, the RBA have built their own version of a financial conditions index in recent years which leans far more heavily into funding spreads and the pace of various lending aggregates. Their index is by definition more backward looking than our approach of calibrating key financial market instruments to explain how they will impact future economic growth and in turn inform the appropriate future course for policy. In short, we believe the RBA are likely missing the degree to which financial conditions are tightening in real time. In particular, the RBA’s assessment that “financial conditions have tightened a little this year, but the extent to which monetary policy is restrictive is uncertain” is almost certainly wrong. We believe the current level of financial conditions post the RBA hike is now at the most restrictive in 12 years. Contrast this to mid-2025 when we estimated Australian financial conditions were at a neutral setting. At that time, the RBA seemed to be in agreeance, but the gap between how we and RBA currently view financial conditions could hardly be more different.

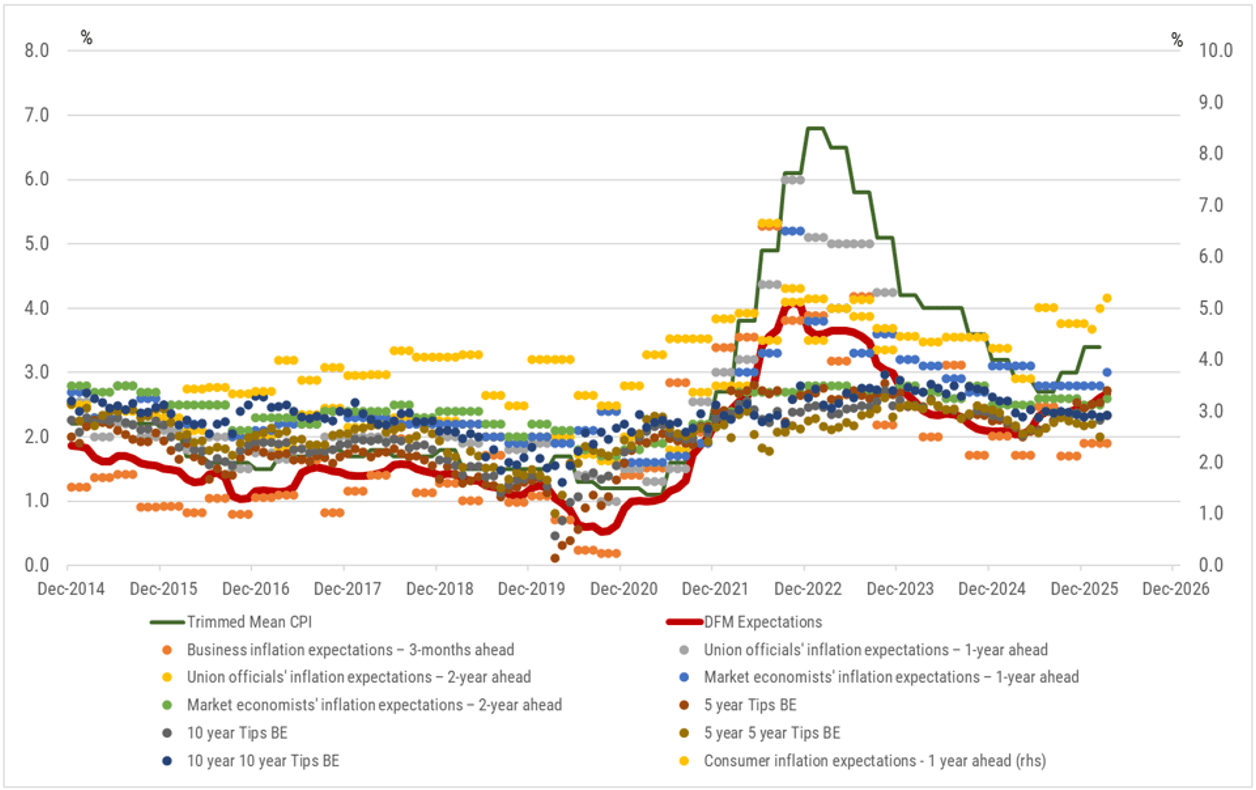

The RBA has relied heavily upon the view that inflation expectations are rising, particularly near-term inflation expectations, to justify yesterday’s hike. The RBA publishes an admittedly small number of the inflation expectation data that they follow on their website. We also supplement those measures with additional measures of inflation expectations from the TIPS market and use a similar model to the US Federal Reserve to extract the common signal from the data (see Figure 5).

Figure 5. Common inflation expectations – Dynamic factor model

Source: Yarra Capital Management, March 2026.

The RBA appears to be referring to a lift in consumer inflation expectations and has also recently referenced two-year inflation expectations from the TIPS market. The focus on short-dated breakeven inflation securities is curious given they are quite illiquid instruments, and it is well known that two-year breakeven inflation securities in major economies largely map oil price moves. In our view, there is little signal and significant noise from these instruments.

In terms of consumer inflation expectations, the primary measure cited by the RBA comes from the Westpac-Melbourne Institute measure. There has been a modest uplift in this measure, but these surveys suffer from several flaws. Firstly, many consumers have a poor grasp of what inflation actually is. Secondly, responses often reflect personal experiences (such as petrol prices or grocery bills) rather than a broad sense of economy-wide price changes. Thirdly, consumers’ views are also heavily influenced by recent price movements or media headlines, leading to volatile short-term responses rather than stable, long-term expectations. As a result, consumer inflation expectations tend to be noisy, erratic, and poorly correlated with actual future inflation outcomes. Indeed, prior research papers from the RBA have pointed to similar conclusions.

Other than via these two relatively flawed measures, we simply can’t see any material lift in inflation expectations in Australia or the USA at present. It may come in time, but we simply can’t see it in the data. The RBA seems to have responded to an anticipated lift in inflation expectations whilst missing a broader turning point in the economic cycle. Furthermore, choosing to tighten into large and persistent exogenous economic shocks could well prove to be one of the biggest policy errors the RBA has made in the inflation targeting era

Expectation shocks, oil price shocks and policy errors have historically been three of the most important causal forces on economic recessions. How many of these do you count?

0 Comments