David Gilmour, Portfolio Analyst & ESG Specialist, looks at the challenges for Australia to reach net zero emissions by 2050.

When we think about decarbonising Australia, switching off coal-fired power stations and replacing with solar and wind farms generally comes first to mind. After all, a plume of steam billowing from a giant chimney is evocative imagery – even if CO2 is invisible. But if we aspire to reaching net zero by 2050, we need to discuss the other 66% of Australia’s emissions.

It’s true that the electricity sector is the largest component of Australia’s GHG emissions, at 179Mt in 2019. But with Australia’s emissions totalling 530Mt in the year, it only generates 34% of our total output. The remaining two-thirds – which doesn’t get enough attention – comprises a mix of Industrials (31%), Transport (19%), Agriculture (13%) and Buildings (4%) (refer Chart 1).

Industrials’ emissions are largely generated through direct combustion (on-site energy needs), Industrial processes (e.g. by-product of manufacturing chemical and metal products) and fugitive emissions (e.g. flaring and venting of methane).

It’s also worth noting that the largest component of Australia’s emissions reductions to date have come from Land Use, Land-Use Change and Forestry (LULUCF), which has turned negative in recent years due to lower land clearing and removals from reforestation efforts. If we exclude LULUCF and electricity, Australia’s CO2 emissions have actually risen 13% since 2005.

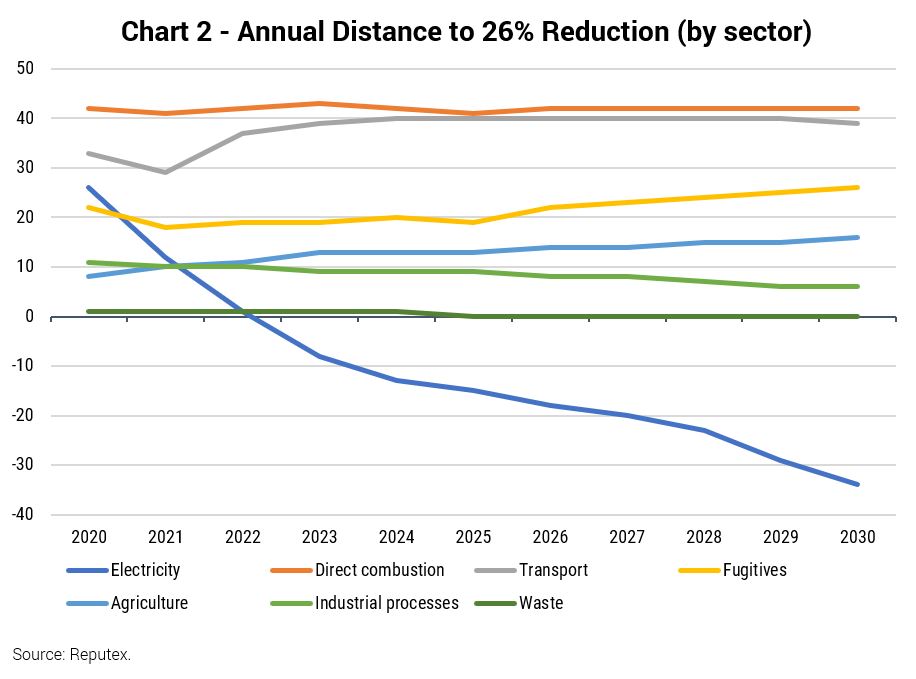

And while electricity has a crucial role in helping these other sectors decarbonise – a clean grid is needed for charging electric vehicles and electrifying home appliances, for example – it cannot shoulder the burden alone. Moreover, electricity is the “low-hanging fruit” on Australia’s path to emissions reduction. Not that it’s at all clear from the federal government’s plans, since Australia’s 2030 target for emissions to fall by 26-28% on 2005 levels relies heavily on the electricity sector, with other sources expected to stay flat or even rise (see Chart 2).

With pressure ratcheting up ahead of the UN Climate Change Conference of the Parties (COP26) in Glasgow in November, the federal government appears set to commit to net zero by 2050. This is not as significant as it sounds; all states and territories and 54% of the ASX100 have already made the pledge. But it does make Australia more accountable on the global stage. And, just as companies are increasingly scrutinized by investors on emissions pathways following net zero commitments, Australia will face more pressure on its 2030 target – where it is fast becoming an outlier.

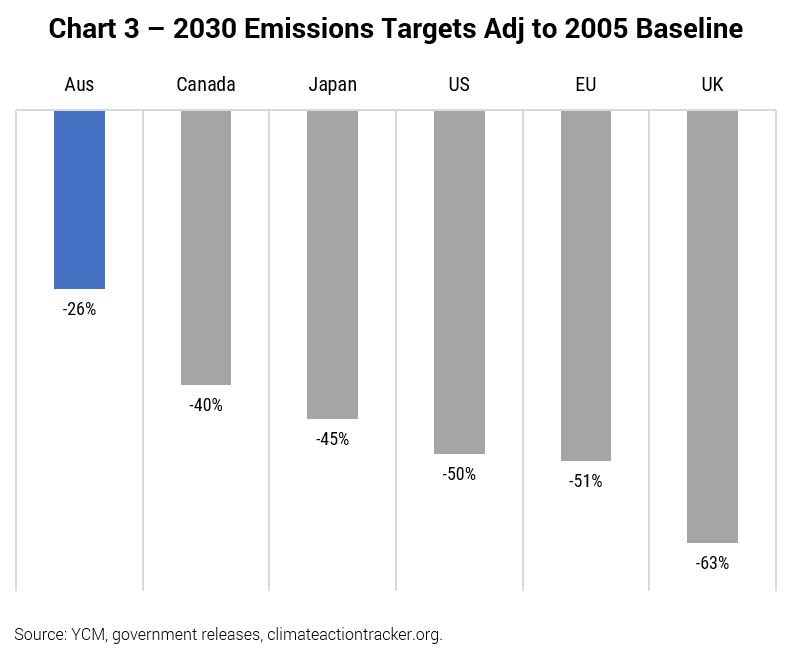

OECD countries are ramping up their 2030 targets (refer Chart 3) at a rapid pace: the US at -50-52% (on a 2005 baseline), the UK at -68% (on a 1990 baseline) and Japan, our 2nd largest trading partner, at -45% (on a 2013 baseline). For context, the Intergovernmental Panel on Climate Change (IPCC) calls for reductions of 45% by 2030 to limit warming to 1.5°C, while the International Energy Agency’s (IEA) Net Zero Pathway has emissions falling by nearly 40% between 2020 and 2030.

In our view, it is only a matter of time before the federal government tightens its 2030 target to levels consistent with Australia’s international peers. To meet such obligations, we need a more robust policy framework that incentivizes sectors – outside electricity – to reduce emissions within the limitations of their industry, And, importantly, one that penalizes those which do not.

The Grattan Institute’s latest report into the Industrials sector, for example, asserts that significant cuts (in the order of ~10%) could be achieved via technology that is readily available now: building renewables on-site, managing fugitive emissions through flaring, upgrading equipment and switching fuels (e.g. from coal to gas). It’s important that we utilize every tool at our disposal, recognizing that fossil fuels (i.e. natural gas) will still be required to maintain an orderly transition.

We continue to monitor our portfolios and the wider investment universe for companies where transition risk is not fully appreciated, and larger emissions reductions will be required as policy settings tighten further. We see few winners but a long list of losers in the ASX: without adequate decarbonization strategies, many companies will be forced to either raise prices (in the hope they can pass through growing emissions liabilities (Australian Carbon Credits are up 87% CYTD)) or have their margins crimped.

We are positioning our Australian Equity portfolios to benefit from winners of the carbon capex cycle where we believe high expectations have not run ahead of fundamentals. While we are more neutral towards lithium given its recent rally, we see latent value in copper producers, with the commodity an essential component in electric vehicles and renewable energy systems. We have recently initiated positions in Sandfire Resources (SFR), OZ Minerals (OZL) and 29Metals (29M).

0 Comments